Economic and technological factors

You are reading the chapter on "Economic and technological factors" of the report "Shaky China - Five scenarios for Xi Jinping's third term". Click here to go back to the table of contents.

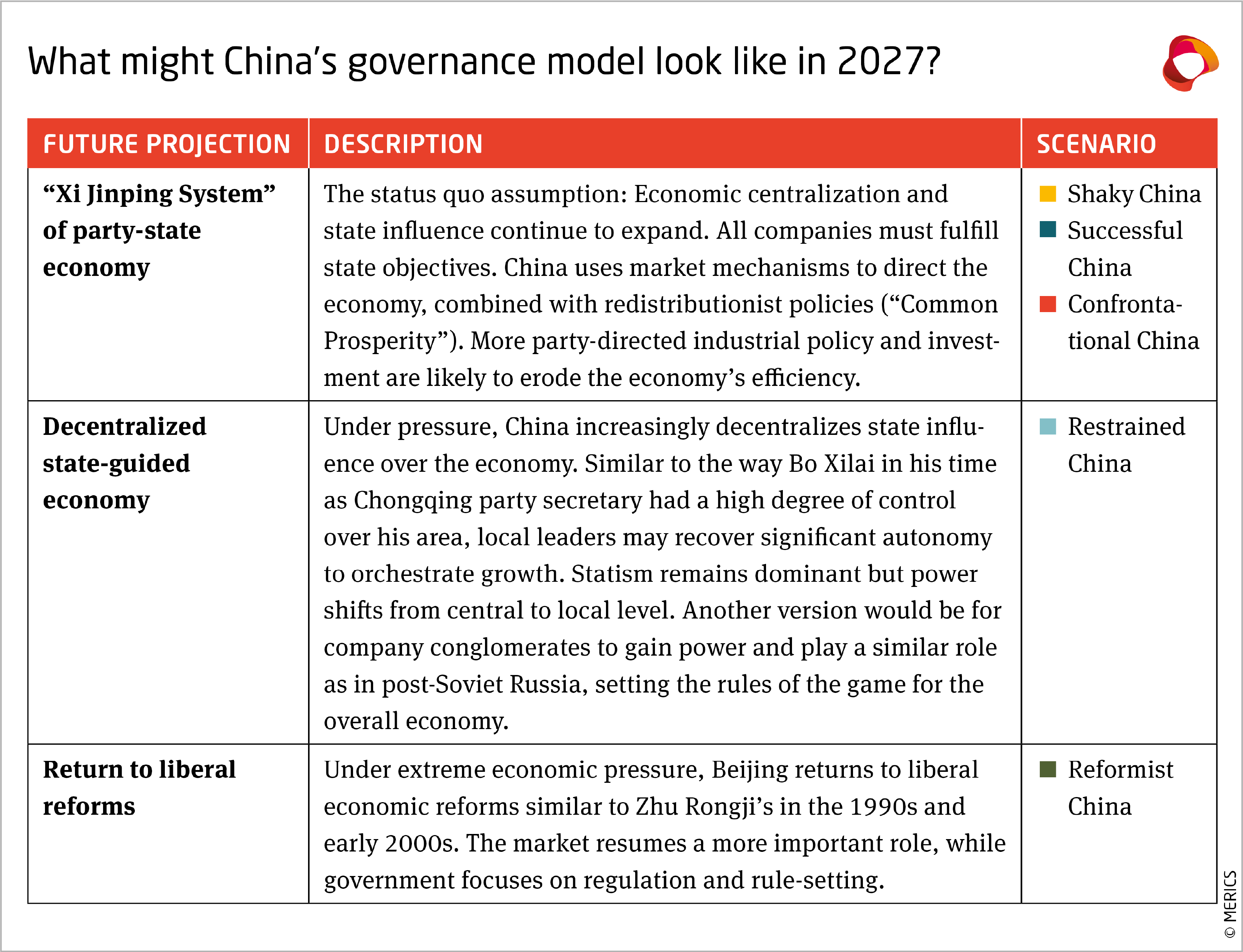

China’s economic governance model

Status quo

In recent years, China has become more centralized. Statism has got stronger, at the expense of the private sector. The government now adopts a ‘whole nation’ approach to development in which private companies must serve state goals. Traditional designations like ‘state-owned enterprises’ versus ‘private enterprises’ are increasingly unimportant under Xi’s party- and state-guided system.

Drivers and dynamics

The external policy environment is highly unpredictable, given unfolding rifts between China and the West over trade and technology, and unity among G7 nations over the Ukraine war. China’s technology sector crackdown, which hobbled a private-sector-dominated growth driver, shows how distinctions between private and state are blurring. Instead, all firms are now charged with fulfilling state objectives. Market oriented reforms are taking a back seat, amid greater emphasis on resilience, self-sufficiency and stability.

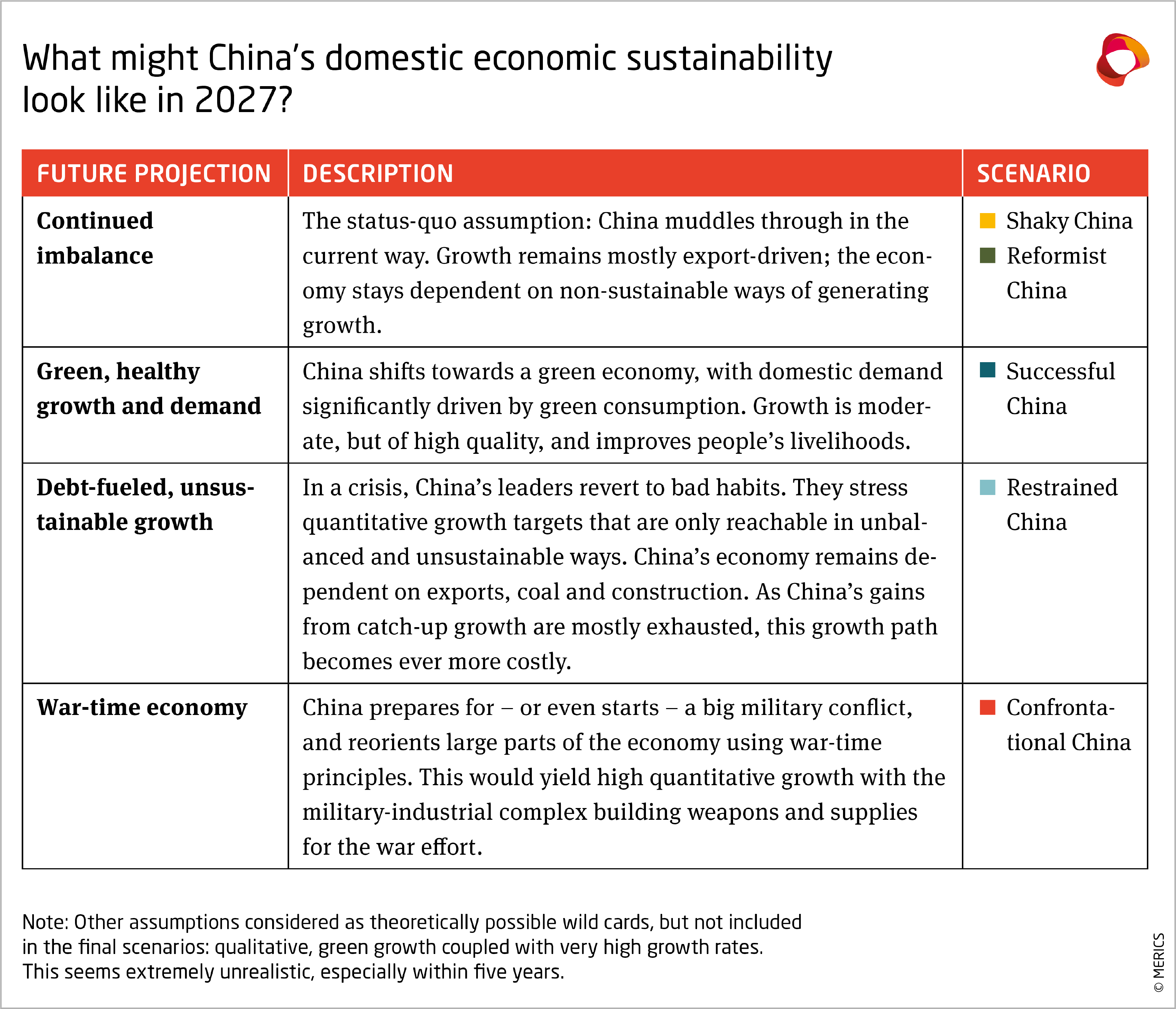

China’s domestic economic sustainability

Status quo

China is struggling to shift towards a more sustainable development model driven by consumption and innovation. Whenever things get hard, the government keeps returning to bad habits, resorting to heavy supply-side stimulus to boost stalling GDP growth, though in the last decade it has become slightly more mindful of financial risk build up.

There is wide consensus that China’s period of relatively easy catch-up growth is ending. China’s current growth model, fueled largely by exports, investment and debt, is not sustainable. The government has long called for a shift to an economy that is more driven by domestic demand, but it has failed to give up the kind of state control the current model allows. Any such change implies leaving a larger share of wealth to consumers, who might not spend their incomes as Beijing wants them to.

Drivers and dynamics

The party-state’s declared wish to overcome long-standing structural challenges is at odds with how Beijing generally intervenes in the economy. In his 20th Party Congress report, Xi Jinping was explicit about tackling oft-mentioned key problems, such as reducing inequality, strengthening SMEs, reforming pensions, promoting regional development, and liberalizing China’s capital account. This begs the question of whether Xi’s third term can prove itself different from so many previous generations of leadership. Will any of these goals finally be realized?

Xi will have to overcome many of the challenges that stalled past reform efforts, such as strong vested interests, a perennial focus on stability, the many real risks that could undercut development, and certain factors unique to China’s style of policymaking and implementation. However, in a third term, an increasingly powerful and authoritarian Xi could use his unquestioned strength to push an agenda through, no matter the vested interests or risks to stability. Similarly, his exclusively loyalist politburo may be able to hold frank conversations that wouldn’t happen if ‘rivals’ listened in. Or it could just as easily become an echo-chamber of yes-men.

Finally, Xi’s grip on power may give him the best opportunity to advance the hard reforms that China needs. However, Xi will have to do so amid unprecedented challenges not faced by his predecessors. At home, Xi faces slower growth and less demand for more infrastructure. Meanwhile, the many, complex risks from abroad include escalating tension between Beijing and Tokyo, tensions over Taiwan, and with the United States and EU (to name just a few).

China in the global economy

Status quo

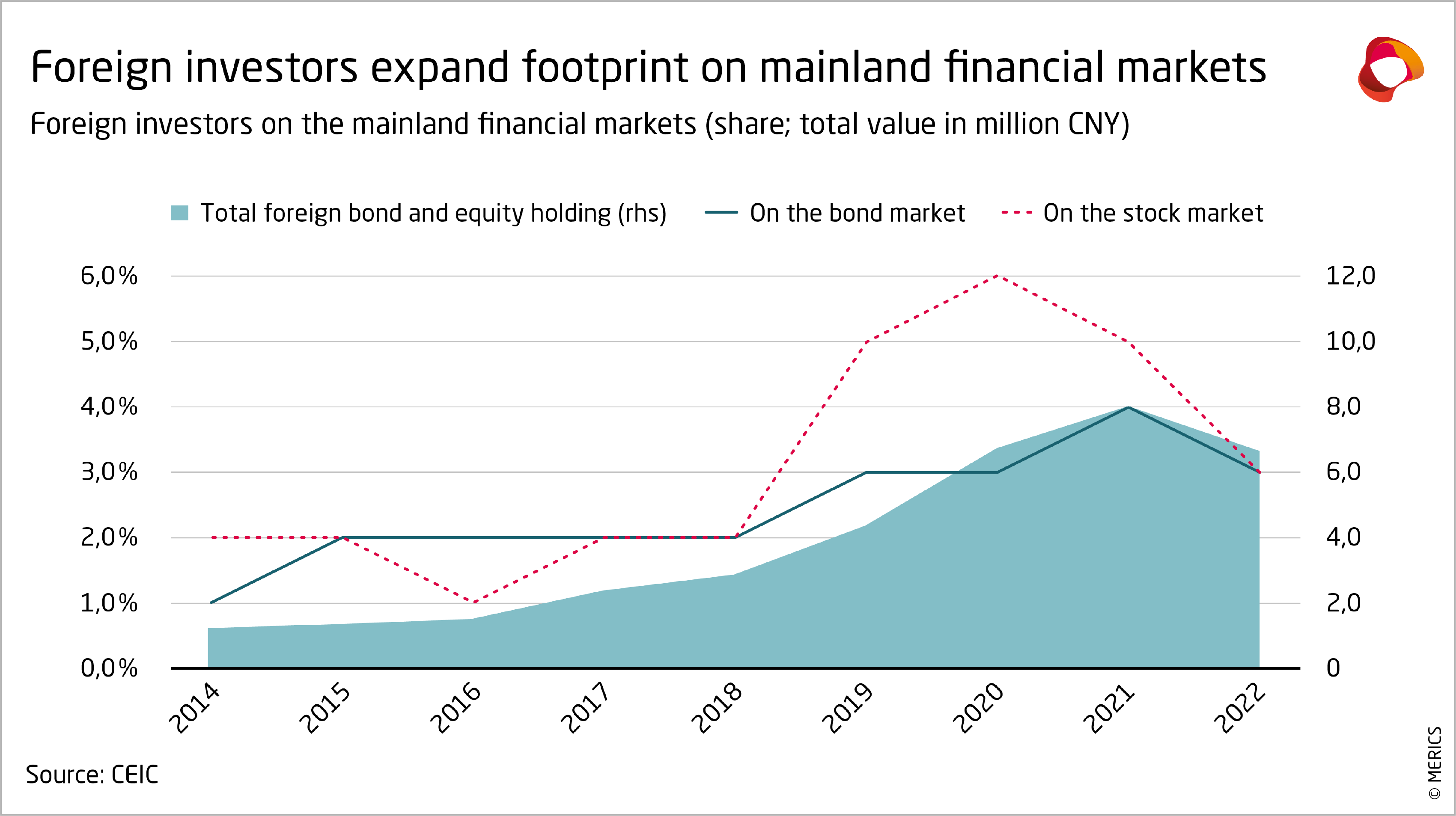

China continues its slow upgrading away from low-value added products, helped by having more competitive domestic companies, and regional value-chains. China’s asymmetric, mercantilist integration into world trade continues to spread, even as the relative importance of foreign trade to China’s economy is decreasing. China has strengthened its position as the world leading trade powerhouse, even in the face of US restrictions on trade and technology exports. Neither US-led restrictions nor Beijing’s own efforts to rebalance the country’s economy towards domestic consumption have dented the growth of Chinese exports, which now stand at almost 20 percent of the global export total. As imports have been less dynamic, China’s external trade surplus has reached USD 900 billion for goods alone.

On the financial side, China has slowed its investments in developing countries. Meanwhile, China has become the focus of hot-money inflows and large scale foreign direct investments (FDI). In 2021, FDI reached a new peak of USD 340 billion, thanks to market opening measures carefully targeted at large firms in priority sectors where China lacks know-how. China seems to have returned to its old practice of recycling those net inflows of hard currency into US treasury bonds. This time, the build-up is not conducted by the central bank to the benefit of the official FX reserves, but by state-owned commercial banks, fueling suspicions of an unofficial mandate to conduct stealth state interventions on the FX markets.

Drivers and dynamics

China’s economic security concerns increasingly impact its role in the global economy. China’s self-sufficiency drive brings pressure to localize, so as to reduce dependency on foreign technology. China’s role in global supply chains has been impacted by supply chain shocks (due to strict Covid controls until late 2022) and by wider decoupling dynamics.

China’s centrality to trade globalization – in terms of scale – is likely to slowly decrease, while value-chain upgrades and regional integration will increase. Strict capital controls will limit the yuan’s position in global finance. Trade tensions and systemic competition in third markets will put more hurdles in front of China’s internationalization efforts and could bring a backlash from Western countries. The discussion on trade in most advanced economies has shifted away from growth and efficiency towards securitization, combined with a more assertive stance towards China. Discussion in China mirrors these concerns, but with a clear focus on how to attract high-quality foreign investments in prioritized sectors and develop self-sufficiency in multiple sectors. Chinese exports cannot be expected to continue the same strong growth as over the past years, given the impact of inflation on consumption in the main destination markets for Chinese products. Still, growing involvement in regional value-chains and slow upgrading on the back of targeted opening up and trade agreements will likely continue.

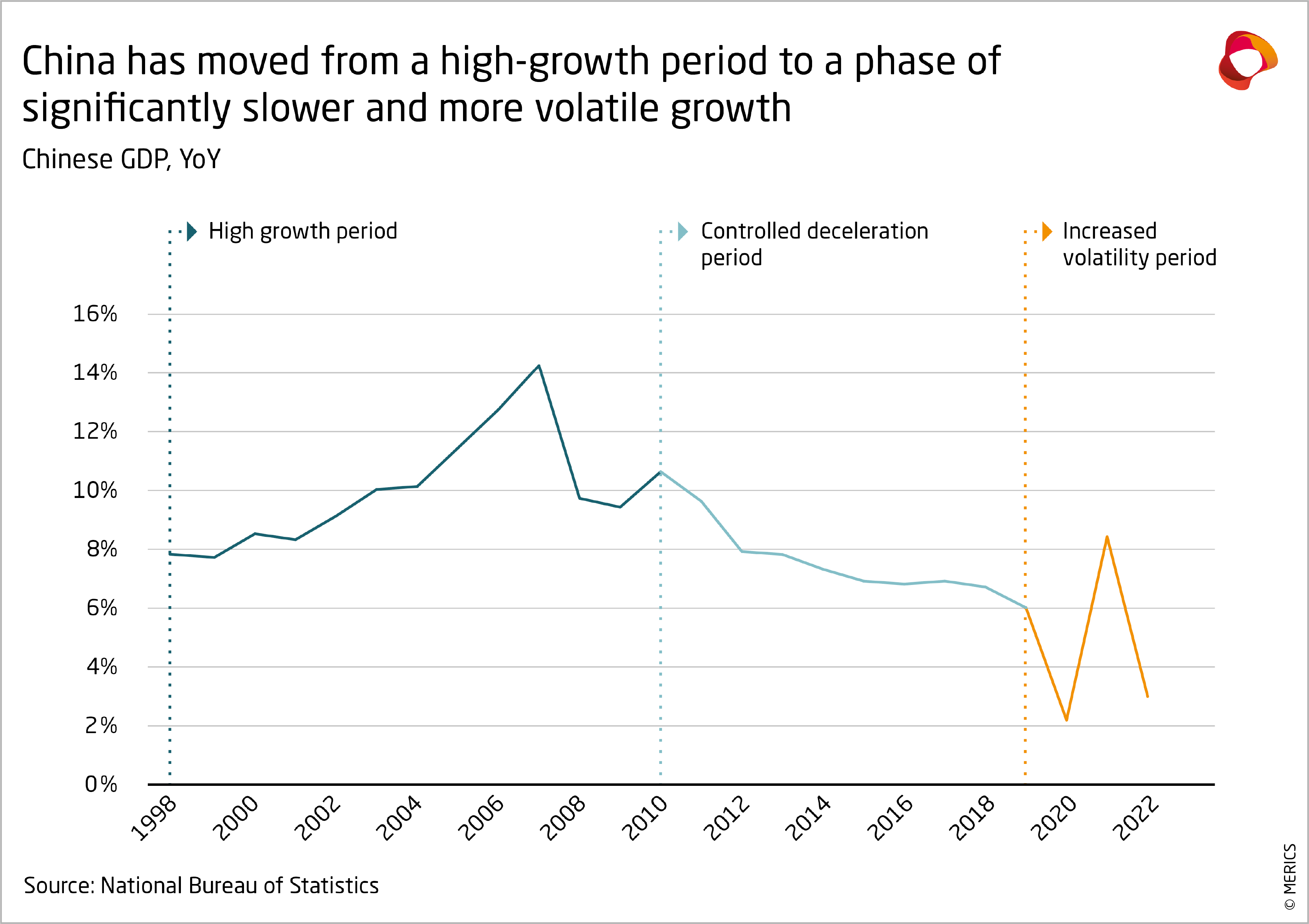

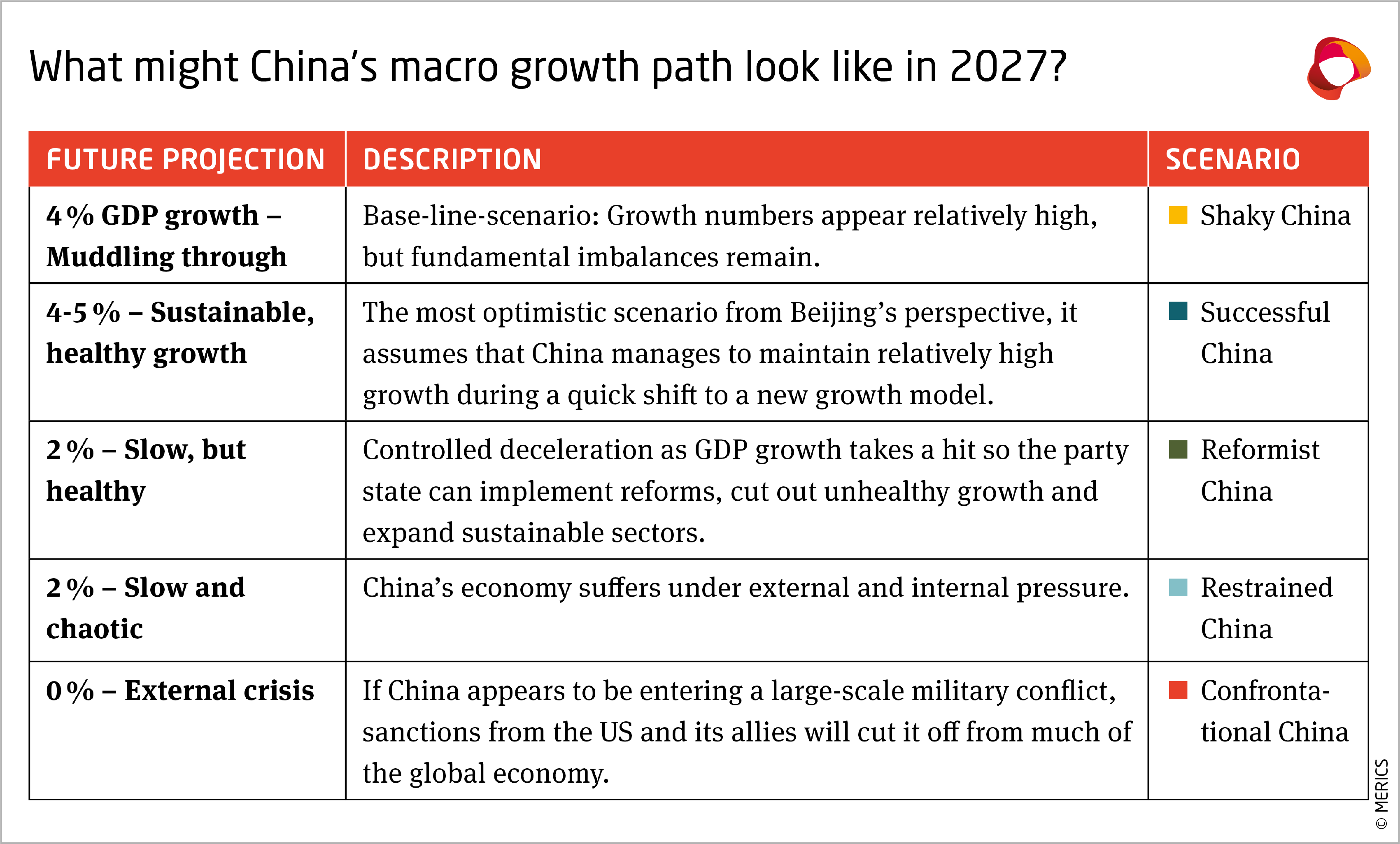

China’s macro growth path

Status quo

China is trying to change its growth model, shifting to a controlled deceleration after 40 years of high growth and entering a period of increased volatility. Growth numbers get much attention, but only tell a small part of the story. Growth composition is more important. Since at least 2012, Beijing has been trying to exit a debt and real-estate fueled growth cycle in favor of a more sustainable model that is innovation-intensive and consumption-based. It has had limited results. Beijing has tried hard to limit debt, especially after 2016. Those efforts seem to have paid off, stabilizing the debt-to-GDP. However, the pandemic response reversed some of this progress. Regulators have made some substantial gains in bringing more market forces into China’s financial markets and improving the business environment (especially on intellectual property and anti-monopoly). More recently, regulators have tightened the screw on the real-estate market, curbing the sector to a point that appears unsustainable for the overall dynamics of the economy. However, the broad imbalances of the Chinese economy remain and may well have increased.

Drivers and dynamics

The era of catch-up growth is coming to an end. Beijing’s standard recipe against economic slumps has been to roll out massive stimulus to boost GDP growth, while juggling financial risk build-up. Now, in a more volatile period, downward pressures on the economy are amplified by stagnating reforms and mounting structural issues. These include an ageing population, the top-heavy role of real-estate in the overall economic mix, the lack of sustainable public finances and low productivity.

Growth still relies on construction, state-driven investments, and exports, while consumption and entrepreneurs are still constrained. The flurry of tighter rules and enforcement in recent years, coupled to the erratic zero-Covid policy and a growing emphasis on ideology, has depressed those Beijing most needs in order to pursue its new development model, namely entrepreneurs and households. The lack of substantial pro-social reforms has impeded any rebalancing towards domestic demand, as households prefer to save. State-owned enterprise reform has also stalled over the years. The prioritization of security over growth does not bode well for sustainable growth.

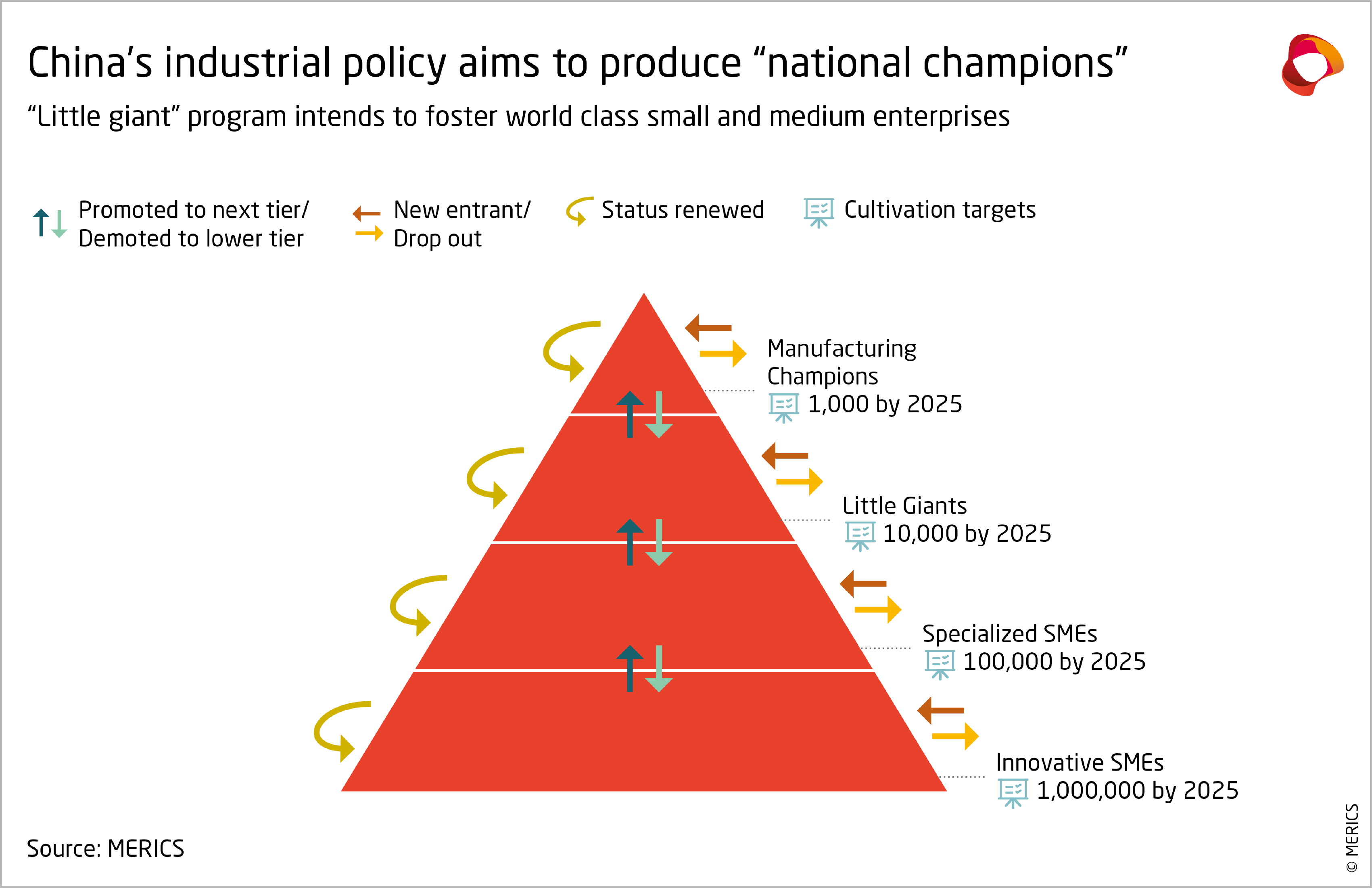

China’s technological independence

Status quo

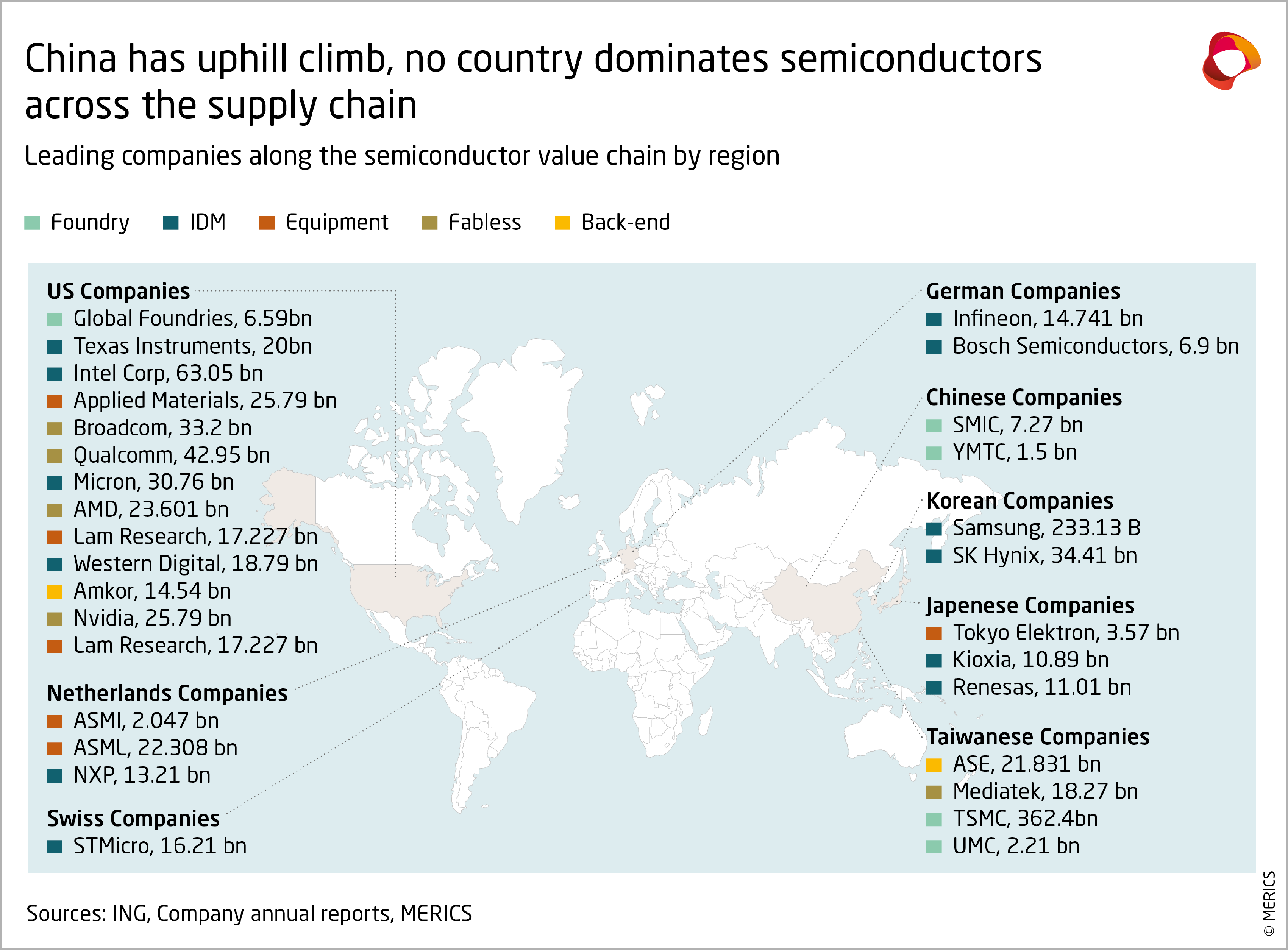

China’s policy aims for self-sufficiency by 2035. Although already less dependent on foreign technology than Germany, China’s deficits are particularly high in strategic, high-tech sectors. In 2017, the government identified 35 chokepoints, including advanced lithography machines for making microchips. Beijing is willing to incur significant costs to nationalize technology. It pushes China’s homegrown Kylin computer operating system, wants to replace all government computers with domestically manufactured ones, and has huge state guidance funds for chips and other key tech. However, this government-led effort is not without problems. Chip sector guidance funds were the subject of a major corruption investigation in August 2022. China’s state-driven approach has produced high-profile successes, but it has been rife with abuses and has fallen far short of the government’s stated goals.

Drivers and dynamics

Technological independence has taken on a new urgency for China since the West showed unity in imposing sanctions on Russia. Beijing is trying to break the 35 chokepoints, and also to establish its own chokepoints to create a system of mutually assured destruction. The United States and EU are developing new tools to limit tech transfer to China, concerned with items such as cutting-edge semiconductors and machinery that would allow China to advance its own semiconductor industry. In October 2022, the United States unilaterally imposed export restrictions on a wide range of products across the chip supply chain. After hesitating, both Japan and the Netherlands, which are the other big players in semiconductor manufacturing equipment, have implemented similar restrictions. These target high-tech semiconductors and the machinery to make them. China’s self-sufficiency drive seems sure to accelerate, especially as fresh rounds of export restrictions are likely on quantum, green technology and biotech.

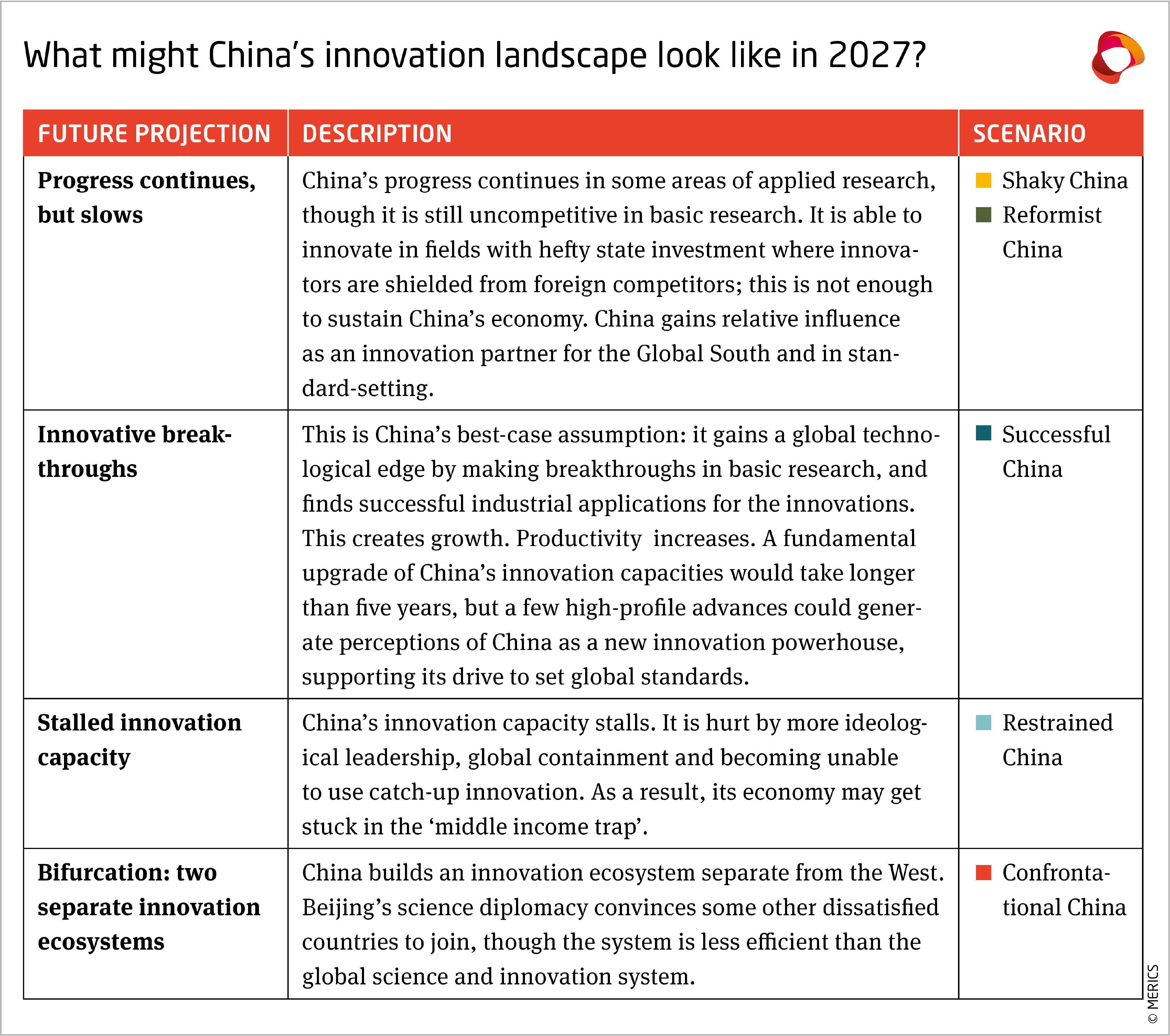

China’s innovation capacity

Status quo

China is leading the world in quality academic papers and patents, and has tech successes in high-speed rail, ICT (5G), digital tech (AI, TikTok), green tech (PV, NEVs, batteries, UHV), quantum and (some) biotech. Most successes are in applied rather than basic research. China is investing hugely in its innovation capacity, taking a state-driven approach. This progress is costly and by some accounts uneconomic; productivity may actually be declining.

Drivers and dynamics

China’s government is once again politicizing all walks of life, including innovation. All inventions are nationalized, and firms are supposed to focus on dual-purpose technology and on releasing the economic chokepoints Beijing has identified. China has reorganized its innovation system across an innovation chain, seeking to take breakthroughs from basic research to commercialization in a shorter time. China’s past innovation growth rested heavily on access to foreign talent, know-how and investment, all of which have been made more difficult since the zero-Covid policy accelerated China’s decoupling from the world. Since China reopened in late 2022, it is unclear how far foreign involvement is welcome in China’s innovation and how far foreigners are willing to keep contributing to it, given the conversations around research security and China as a systemic competitor in Europe, and even more so the United States.

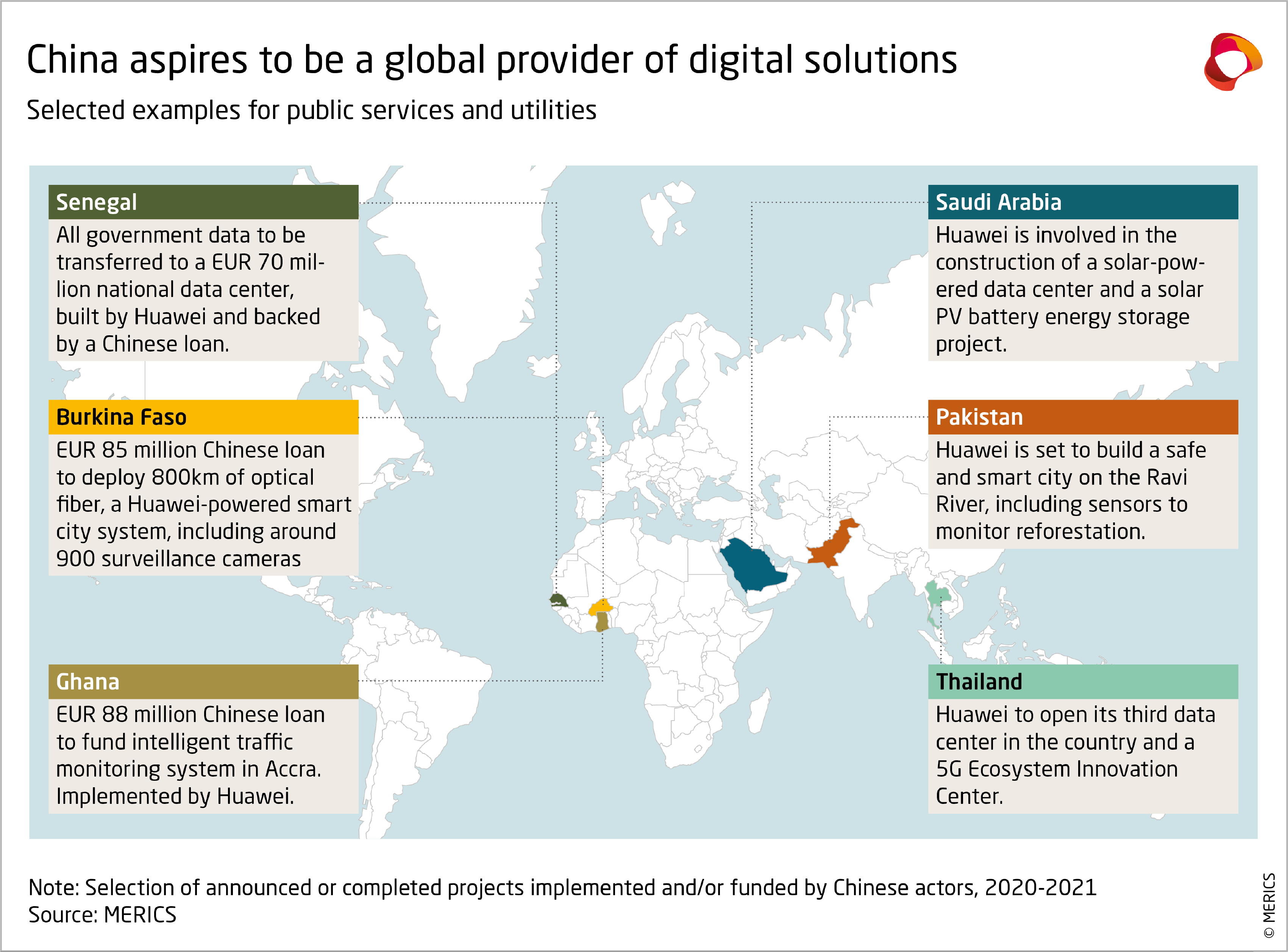

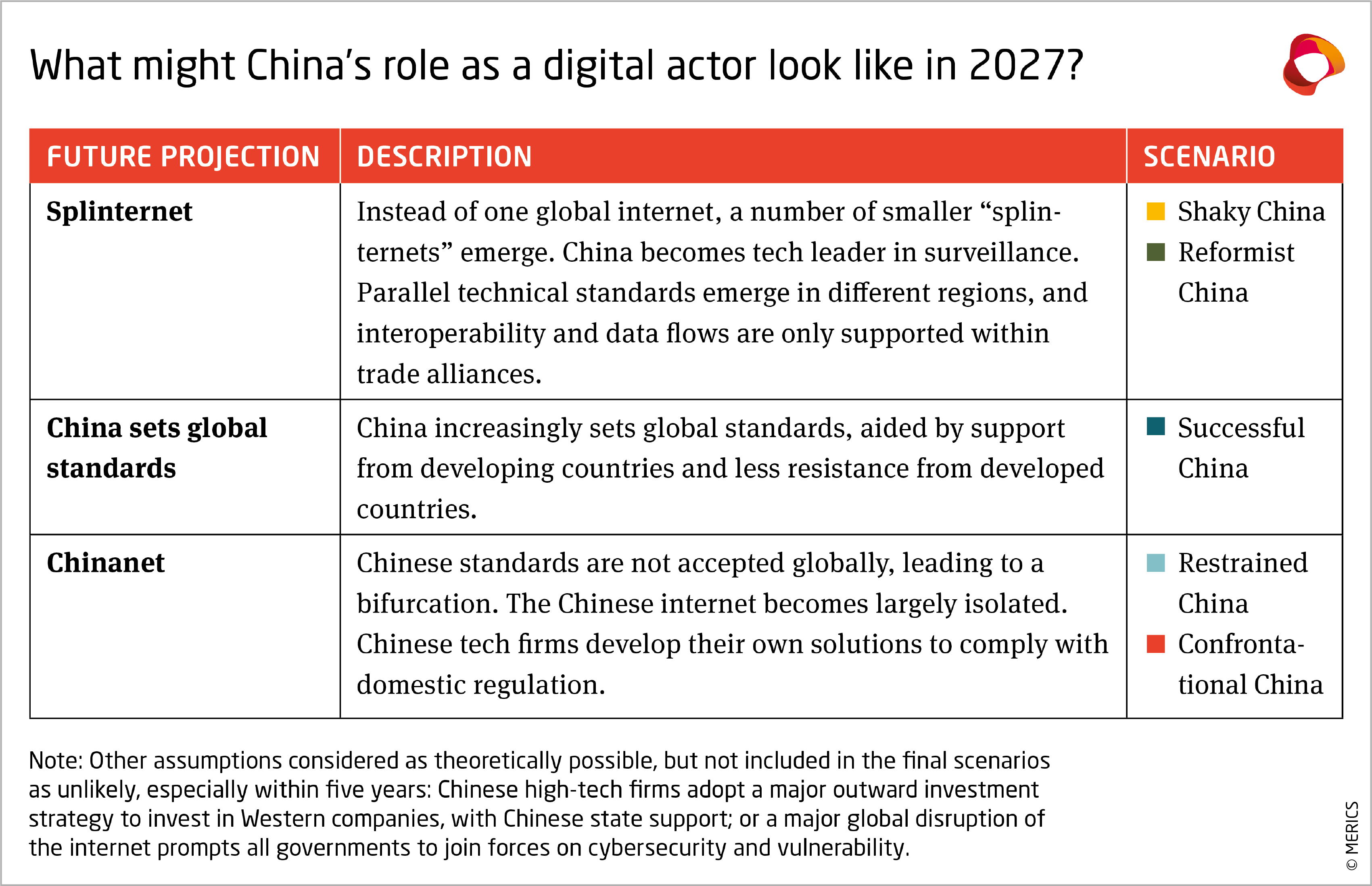

China as a digital actor

Status quo

China has world leading technology giants in Internet, ICT equipment and AI, such as Huawei and Bytedance. Chinese digital infrastructure and products span the globe, with a strong footprint in developing and emerging economies. Only advanced economies have put restrictions on China’s digital infrastructure and products, and these are narrow in scope. China is developing its cyber and digital governance model. The model’s top priority is the protection of regime security from threats emanating from online information flows. China is engaged in pro-active cyber diplomacy, and sees the Fourth Industrial Revolution as an opportunity to claim global leadership and project power. In international cyber forums, China is seeking to position itself as a champion of developing countries and for nation states to have a greater role in standard-setting.

Drivers and dynamics

Beijing seeks advantages from tech firms’ global expansion, creating geopolitical, security and human rights risks. Major Chinese ICT firms such as Huawei export their technology, often funded by the Chinese government. In doing so, they push for new protocols that are designed for censorship and application-specific networking, i.e. allowing content discrimination. China is active in standard-setting, especially in ICT, where it pushes for a greater role for nations in standard-setting, going against the multi-stakeholder model of internet governance. China and the EU are increasingly competing for their vision of digital development in the world, with China’s Digital Silk Road and the EU’s Global Gateway. China’s vision of the Internet is increasingly at odds with the Western vision of the Internet, with application-specific networking and content discrimination baked in. With China’s export of surveillance technology and Internet technology, China’s vision is becoming embedded in the backbone of the Internet, especially in the Global South.

You were reading the chapter on "Economic and technological factors" of the report "Shaky China - Five scenarios for Xi Jinping's third term". Click here to go back to the table of contents.

Author

Bernhard Bartsch

Director External Relations