picture alliance / CFOTO

Report

Debatten über prekäre Jobs, den Alltag in Taiwan und Chinas Rolle in der Welt

![]() Diese Analyse erschien in der Reihe China Spektrum, ein gemeinsames Projekt des China-Instituts der Universität Trier (CIUT) und des Mercator Institute for China Studies (MERICS). Das Projekt wird ermöglicht durch die Förderung der Friedrich-Naumann-Stiftung für die Freiheit. Mehr erfahren Sie hier.

Diese Analyse erschien in der Reihe China Spektrum, ein gemeinsames Projekt des China-Instituts der Universität Trier (CIUT) und des Mercator Institute for China Studies (MERICS). Das Projekt wird ermöglicht durch die Förderung der Friedrich-Naumann-Stiftung für die Freiheit. Mehr erfahren Sie hier.

Auf einen Blick

China will seine Rolle als aufsteigende Weltmacht verteidigen. Doch dafür braucht der Parteistaat eine stabile Basis. Das Wirtschaftswachstum hat sich jedoch verlangsamt und die öffentlichen Finanzen sind angeschlagen. Neben einer Reihe von Förderprogrammen für die Privatwirtschaft sollen flexible Arbeitsverhältnisse dabei helfen, die hohe Jugendarbeitslosigkeit in den Griff zu bekommen. Damit die Bevölkerung trotz innenpolitischer Herausforderungen hinter der Partei und ihrem Kurs steht, setzt die Regierung auch auf neue Regeln: ab dem nächsten Jahr gilt ein neues Gesetz zur patriotischen Erziehung.

Chinas Zukunftsvorstellungen

"Flexibel Beschäftigte" - Rentensystem vor neuen Herausforderungen

Angesichts der fortschreitenden Überalterung sehen Expert:innen einen dringenden Handlungsbedarf für eine Rentenreform, insbesondere für sogenannte „flexibel Beschäftigte“, zu denen neben einfachen Arbeiter:innen auch Influencer:innen zählen. Sie erhalten kaum staatliche Unterstützung und sind besonders von Altersarmut bedroht. Expert:innen diskutieren strukturelle Probleme und Lösungsstrategien zur besseren Verteilung der Verantwortung für die Altersvorsorge zwischen Individuum, Staat und Unternehmen.

Chinas digitale Transformation

Xiaohongshu - eine schmale Brücke über die Taiwanstraße

Die chinesische Lifestyle-App Xiaohongshu ist für Chines:innen und Taiwaner:innen eine der wenigen verbleibenden Plattformen, um miteinander zu kommunizieren. Die Auswertung von über 900 Fragen chinesischer Netizens an Taiwaner:innen zeigt, dass die Neugier über das Alltagsleben und Taiwans Popkultur im Vordergrund stehen. Fragen zur Politik und Geschichte werden – in geringerem Umfang – aber auch gestellt. Im Vergleich zu anderen Plattformen finden sich hier weit weniger nationalistische Kommentare. Doch im Vorfeld der Wahlen in Taiwan wird auch dieses Medium von beiden Seiten skeptisch beäugt.

Chinas Rolle in der Welt

Online-Länderranking - Stolz auf China, aber auch Bewunderung für die USA

Die chinesische Regierung und Staatsmedien preisen China regelmäßig als aufstrebende Weltmacht. Da verwundert es nicht, dass die Mehrheit chinesische Netizens auf der Plattform Zhihu die Frage, welches das „großartigste“ Land der Welt sei, mit „China“ beantwortet. Direkt darauf folgen allerdings die in China eigentlich viel kritisierten USA und weitere westliche Länder. Auch Deutschland sichert sich einen Platz auf dem Treppchen. In den Kommentaren mischen sich offene Bewunderung für das eigene Land und die Errungenschaften westlicher Staaten mit versteckter Kritik und Satire über China und weitere autoritären Regime.

Einleitung

Das alles ändert nichts an der aktuellen Krise auf dem Immobilienmarkt und der niedrigen Geburtenrate. Insbesondere in der Sozialpolitik stehen China eine Reihe struktureller Herausforderungen bevor, von wachsender Ungleichheit bis zu Finanzierungslücken im Sozialsystem. Das Rentensystem kann kaum mit dem demographischen Wandel mithalten, die Flexibilisierung des Arbeitsmarktes erschwert die Absicherung zusätzlich. Das Dritte Plenum wird zeigen, ob die Partei bereit ist, diese Probleme anzugehen.

Staats- und Parteichef Xi scheint zur Sicherung des gesellschaftlichen Zusammenhalts eher auf politische und ideologische Kontrolle als auf Reformen zu setzen. In den vergangenen Monaten appellierte er wiederholt an Parteikader und Beamt:innen, sich auf extreme Szenarien vorzubereiten. Das Ministerium für Staatssicherheit lancierte eine landesweite Kampagne, die vor ausländischer Unterwanderung und Spionen warnt – und kollektive Wachsamkeit beschwört. Im Oktober verabschiedete China zudem ein neues Gesetz zur patriotischen Erziehung, das Anfang nächsten Jahres in Kraft treten wird. Es verpflichtet nicht nur Bildungsstätten, sondern auch alle öffentlichen Behörden und Interessenverbände, die Liebe zum Land und zur Partei durch verschiedenste Maßnahmen zu fördern.

Während sich China ideologisch stärker abschottet, tritt das Land nach außen immer selbstbewusster auf. In einem neuen Weißbuch beschreibt die chinesische Führung ihre Vision für eine globale Zukunft, im Oktober folgte ein Plan für Chinas regionale Außenpolitik und das Verhältnis zu seinen Nachbarstaaten. Ende Oktober feierte China mit einer Reihe internationaler Gäste – darunter der russische Präsident Wladimir Putin – das zehnjährige Bestehen der Seidenstraßeninitiative.

Gleichzeitig reißt der Graben zwischen China und westlichen Staaten immer weiter auf, trotz aktueller Bemühungen Chinas und der USA, wieder ins Gespräch zu kommen. Insbesondere die anhaltende, enge Beziehung zwischen China und Russland, die Weigerung Beijings, die Hamas als terroristische Organisation einzustufen und Auseinandersetzungen um Gebietsansprüche im Südchinesischen Meer erschweren dem Westen die Zusammenarbeit in sicherheitspolitischen Fragen. Nicht zuletzt besteht auch das Risiko einer Eskalation in der Taiwanstraße, wo Beijing seine militärischen Drohgebärden zuletzt verstärkt hat. In Taiwan stehen am 13. Januar sowohl Präsidentschafts- als auch Parlamentswahlen an, die aus China genau beobachtet werden.

Chinas Bürger:innen werden in den Medien und sozialen Netzwerken täglich mit staatlichen Positionen und patriotischen Appellen bespielt. Sie haben nur sehr eingeschränkt Zugang zu internationalen Plattformen. Das offizielle Narrativ dominiert, auch wenn ihm nicht uneingeschränkt Glauben geschenkt wird, wie ein Blick auf Kommentare zu Chinas internationalem Status in sozialen Medien und der Austausch zwischen Festlandchines:innen und Taiwaner:innen auf der Plattform Xiaohongshu zeigen. Trauerbekundungen zum plötzlichen Tod des ehemaligen Premierministers Li Keqiang wurden trotz strenger Überwachung genutzt, um Kritik am politischen Kurs zu äußern. Viele teilten ein Zitat Li Keqiangs von Anfang 2022: „Chinas Reformen und die Öffnung werden nicht enden.“

Chinas Zukunftsvorstellungen

"Flexibel Beschäftigte" - Rentensystem vor neuen Herausforderungen

2023 ist ein Jahr der schlechten Zahlen für China. Neben der steigenden Jugendarbeitslosigkeit und rückläufiger Heirats- und Geburtenraten stellt die zunehmende Überalterung der Gesellschaft China vor eine große Herausforderung. Der Anteil der Über-60-Jährigen an der Bevölkerung liegt derzeit bei etwa 19,8 Prozent (280 Millio- nen) und wird Schätzungen zufolge bis 2040 auf 28 Prozent (und 402 Millionen Menschen) ansteigen.

Das führt zu einer enormen Belastung für Chinas Sozialversicherungssystem, denn die meisten dieser Personen sind in naher Zukunft auf Rentenzahlungen angewiesen. Das reguläre Renteneintrittsalter für Arbeiter:innen liegt aktuell bei 60 Jahren für Männer und bei nur 55 Jahren für Frauen, auch wenn für Beamte und andere Berufe zum Teil mehr Arbeits- und damit Beitragsjahre möglich sind. Angesichts der steigenden Lebenserwartung werden schon lange Strukturreformen des Rentensystems angemahnt. Frauen leiden besonders unter der derzeitigen Lage. Geschlechtsspezifische Probleme wurden in bisherigen Reformen kaum berücksichtigt. Dabei ist die Rente von Frauen im Schnitt 20 Prozent niedriger als jene von Männern.

Gleichzeitig erwachsen in China gerade neue Probleme in der Altersvorsorge, auch vorangetrieben durch das Phänomen der „flexiblen Beschäftigung“ (灵活就业). Diese rasant zunehmende „neue Arbeitsform“ (新就业形态) entwickelte sich in den vergangenen Jahren mit der Digitalisierung und dem Aufkommen der sogenannten „Platform Economy“ (平台劳动者).1 Problematisch ist, dass nur etwa 36 Prozent aller flexibel Beschäftigten in der Grundversicherung für Beschäftigte (职工基本养老保险) registriert sind. Die Grundversicherung ist nur für Angestellte in Unternehmen verpflichtend. Für „flexibel Beschäftigte“ ist die Teilnahme freiwillig.

Anfang 2022 gingen etwa 200 Millionen Menschen in China einer solchen flexiblen Beschäftigung nach, was fast einem Drittel der gesamten erwerbstätigen Bevölkerung entspricht – Tendenz steigend. Die „flexible Beschäftigung“ umfasst ganz verschiedene Tätigkeiten, darunter Kurierfahrer:innen, Influencer:innen und andere Selbstständige, die teils einen hohen Bildungsabschluss besitzen. Unter flexible Beschäftigung fallen aber auch traditionelle Tätigkeiten des informellen Sektors, wie Haushaltshilfen oder Teilzeit- und Vertragsarbeiter:innen – Bereiche, in denen häufig sogenannte Arbeitsmigrant:innen (siehe Infobox) beschäftigt sind.

Dass so viele verschiedene Arbeitsfelder und soziale Schichten unter einem Begriff zusammengefasst werden, erschwert die Diskussion und Erarbeitung politischer Lösungen. Auch chinesische Behörden und parteistaatliche Medien gestehen die fehlende soziale Absicherung von Arbeitnehmer:innen in flexiblen Arbeitsverhältnissen ein.

Arbeitsmigrant:innen

Es sind die Wanderarbeiter:innen, die das Bild der Arbeitsmigration in China bis heute in unseren Köpfen prägen. Ströme von Menschen, die zu Beginn der wirtschaftlichen Reformen seit Anfang der 1980er Jahre auf der Suche nach Arbeit aus den ärmeren Regionen im Westen des Landes in die reichen Küstenstädte im Osten Chinas zogen. In späteren Jahren blieben derartig große Wanderbewegungen aus, stattdessen verblieb die zweite Generation oft innerhalb der Städte oder der Grenzen einer Provinz.

2021 zählte Chinas Nationales Büro für Statistik 385 Millionen Binnenmigrant:innen. Dies entspricht 27 Prozent der Gesamtbevölkerung. Obwohl die chinesische Regierung die Freizügigkeit durch verschiedene Regularien einschränkt, haben sich die Zahlen seit 2010 verdoppelt.

Ein wesentlicher Grund für die ansteigenden Zahlen ist die Diversifizierung der Beschäftigungsverhältnisse dieser Personengruppe. Zwar bestand sie 2022 noch aus über 295 Millionen Arbeiter:innen, aber auch zunehmend aus Digital Nomads und anderen Angestellten mit Universitätsabschluss, die nicht mehr auf einen festen Arbeitsort angewiesen sind und mobil in verschiedenen Teilen des Landes arbeiten können.

Flexibel Beschäftigte sind unzureichend abgesichert – die Gründe sind vielfältig

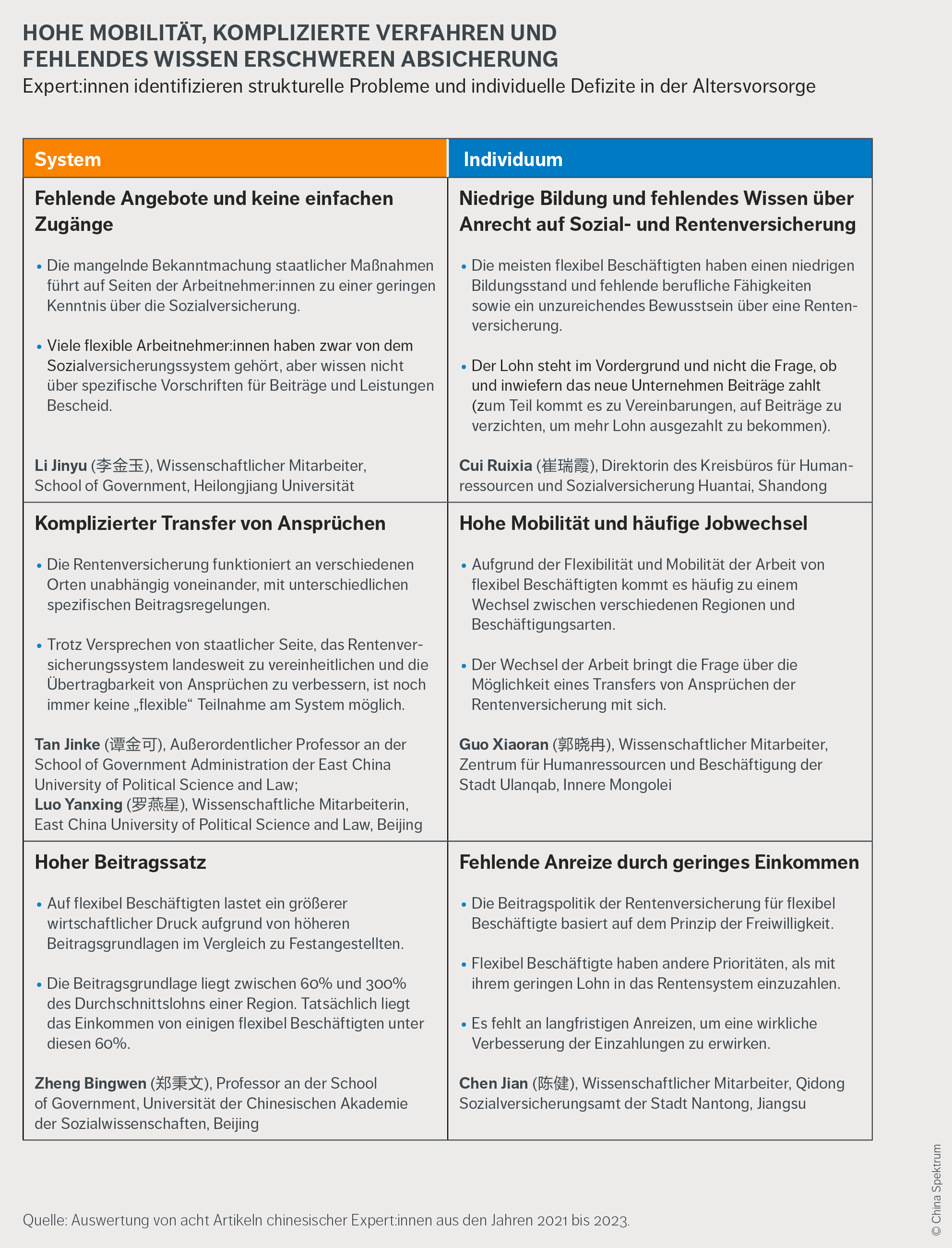

Das Problem der Sozialversicherung für flexibel Beschäftigte wird in den Medien thematisiert und auch von staatlicher Seite zunehmend als ein Problem wahrgenommen. Auch unter Expert:innen wird die Thematik vielfältig diskutiert, wie eine Auswertung von acht Fachpublikationen aus den Jahren 2021 bis 2023 zeigt.2

Einigkeit herrscht vor allem darüber, dass die fehlende Altersabsicherung für den einzelnen flexibel Beschäftigten und damit einhergehend das staatliche Sozialversicherungssystem im Ganzen ein Problem darstellt. Die große Diversität der flexibel Beschäftigten macht eine einheitliche Regelung schwierig. So bestehen große Unterschiede zwischen den Bedürfnissen von Arbeitsmigrant:innen aus ärmeren Landesteilen und Universitätsabsolvent:innen, die als Influencer:innen oder Designer:innen freiberuflich arbeiten.

Die Expert:innen machen verschiedene Ursachen für die fehlende Absicherung der flexibel Beschäftigten aus, sowohl auf staatlicher als auch auf individueller Seite.3 Diese verstärken sich oft gegenseitig. Bei vielen flexibel Erwerbstätigen stoßen ein häufig niedriges Bildungsniveau und mangelndes Wissen über Sozial- und Rentenversicherungen auf fehlende staatliche Angebote und schlechte Zugänge zu Informationen für Beschäftigte. Zudem leiden Arbeitsmigrant:innen mit ihrer hohen Mobilität und häufigen Jobwechseln unter komplizierten Transferverfahren von Sozialleistungsansprüchen in andere Provinzen. Auch gilt für sie trotz eines häufig geringeren Einkommens ein höherer Beitragssatz als für Festangestellte. Daher sind flexibel Beschäftigte oft weniger motiviert, in das Rentensystem einzuzahlen und suchen stattdessen nach Alternativen, um ihr Geld anzulegen.

Während sich Expert:innen in Hinblick auf die Gründe für die fehlende Beteiligung flexibel Beschäftigter an der Rentenversicherung offenbar einig sind, zeigt die Diskussion potentieller Lösungsstrategien unterschiedliche Ansätze. Insbesondere bei der Frage der Verantwortlichkeiten herrscht Uneinigkeit. Die meist kurzfristigen und sich zudem oft überschneidenden Arbeitsverhältnisse erschweren eine klare Zuweisung von Verantwortung an Staat, Arbeitgeber oder Beschäftigte:

- So spricht sich ein Teil der Expert:innen dafür aus, dass der Staat eine stärkere Führungsrolle einnehmen müsse. Dies umfasst die Schaffung rechtlicher Grundlagen genauso wie die Entlastung von Arbeitgebern, indem Rentenauszahlungen durch den Staat übernommen werden. Die entstehende finanzielle Belastung soll über eine zusätzliche Besteuerung der Unternehmen ausgeglichen werden.

- Andere fordern hingegen, die Unternehmen stärker in die Pflicht zu nehmen, da diese oft gezielt Sozialversicherungszahlungen verweigern, um die eigenen Profite zu steigern.

- Weitere Expert:innen sehen die Lokalregierungen in der Pflicht, die Bevölkerung über die Rentenversicherung zu informieren. Hierfür sollen neue Vorschriften und Regeln aufgestellt und die lokalen Beamten bei fehlender Sorgfaltspflicht mit Strafen belegt werden.

- Andere Expert:innen argumentieren, dass sich die Beschäftigten selbst dafür verantwortlich fühlen sollten, Sparpläne zu erstellten und sich über weitere Vorsorgemöglichkeiten zu informieren.

Neben der Zuständigkeitsdebatte finden sich weitere Lösungsvorschläge. Dazu zählen:

- Eine Reform und Umstrukturierung des derzeitigen Versicherungssystems. Diese umfasst unter anderem die Festlegung eines angemessenen Beitragsniveaus und eine Verbesserung der Übertragbarkeit von Ansprüchen über Provinzgrenzen und verschiedene Arbeitsverhältnisse hinweg.

- Die Schaffung neuer Zugänge zu bestehenden öffentlichen Dienstleistungen für flexibel Beschäftigte, zum Beispiel über Apps.

- Spezielle Kurse für Beschäftige über das Rentensystem zur Schaffung eines größeren Bewusstseins über die Wichtigkeit der Einzahlungen.

Die Vielzahl an diskutierten Maßnahmen zeigt die große Komplexität dieses neuen gesellschaftspolitischen Problems.

China benötigt eine umfassende Rentenreform, die neue Arbeitsformen berücksichtigt

Der Fokus der Berichterstattung liegt oft auf Chinas rasantem Aufstieg. Doch die alternde Bevölkerung und strukturelle Probleme im Renten- und Sozialversicherungssystem werden China in den nächsten Jahrzehnten vor große Herausforderungen stellen. Insbesondere Beschäftigte aus der niedrigen Einkommensschicht fallen im derzeitigen Sozialversicherungssystem nach wie vor durchs Netz. Sobald sie durch Krankheit oder Alter keiner Beschäftigung mehr nachgehen und damit unmittelbares Einkommen erzielen können, droht ihnen aufgrund geringer Einzahlungen in das Versicherungssystem der Verlust ihrer Existenzgrundlage. Da auch das staatliche Sozialhilfesystem mit Ressourcenmangel zu kämpfen hat, rutschen diese Menschen in die (Alters-)Armut.

Obwohl die Möglichkeit der flexiblen Beschäftigung derzeit sowohl für die Wirtschaft als auch für die Beschäftigten Vorteile hat, verursacht sie durch fehlende Beitragszahlungen und die Verstärkung der Ungleichheit zwischen verschiedenen sozialen Einkommensschichten sowie den Geschlechtern Probleme für das Renten- und Sozialsystem. Die chinesische Regierung muss daher die überfällige Reform des Rentensystem angehen, um eine nachhaltige gesellschaftliche Entwicklung zu gewährleisten und soziale Verwerfungen einzudämmen. Dies erfordert auch, auf die Bedürfnisse flexibel Beschäftigter aus verschiedenen sozialen und Einkommensschichten einzugehen.

Auch in Deutschland sollte man Chinas mühsames Ringen mit einer alternden Bevölkerung und Sozialreformen nicht auf die leichte Schulter nehmen. Wenn mehrere hundert Millionen Menschen in den kommenden Jahren aus dem formellen Arbeitsmarkt ausscheiden und eine entsprechende Absicherung verlieren, verliert die chinesische Wirtschaft – und damit die Weltwirtschaft – auch kaufkräftige Konsument:innen in der Zukunft.

Neben den wirtschaftlichen Auswirkungen auf die globale und deutsche Wirtschaft steht Deutschland angesichts einer ebenfalls alternden Bevölkerung teils vor ähnlichen Problemen wie China, gerade auch was den Wandel des Erwerbslebens und flexible Beschäftigungsformen angeht. Ein Blick auf die chinesische Debatte zu Reformen des Rentensystems bietet daher viele Anknüpfungspunkte für politische Entscheidungsträger:innen, um mit China zu einem wichtigen Thema im Dialog zu bleiben und zusammenzuarbeiten.

Weiterführende Informationen:

Chinas digitale Transformation

Xiaohongshu - eine schmale Brücke über die Taiwanstraße

„Wie sieht es mit den Löhnen in Taiwan aus? Die Beschäftigungsquote ist hier [in China] so schlecht. Aus meiner Sicht stehen die Löhne und Mieten in keinem angemessenen Verhältnis zueinander”, schrieb am 8. Juli 2023 eine Nutzerin auf der Plattform Xiaohongshu („Kleines rotes Buch“) in einem Chat, wo sich Festlandchines:innen und Taiwaner:innen austauschen.

Solche Kanäle der direkten Kommunikation zwischen Chines:innen und Taiwaner:innen sind ungewöhnlich. Die Beziehungen zwischen der Volkrepublik China und Taiwan werden überschattet von Militärübungen und wiederholten Androhungen der chinesischen Führung, die „Wiedervereinigung“ mit dem Festland notfalls mit militärischer Gewalt herbeiführen zu wollen.

Wie der Besuch der damaligen Sprecherin des US-Repräsentantenhauses Nancy Pelosi im August 2022 zeigte, werden soziale Medien in China beim Thema Taiwan oft von nationalistischen Tönen dominiert. Zwar bot die Plattform Clubhouse, auf der man in Live-Chaträumen zu unterschiedlichen Themen diskutieren kann, im Januar 2021 kurzzeitig einen Kanal, über den Chines:innen und Taiwaner:innen – teilweise zum ersten Mal überhaupt – offen und respektvoll über ihre Wahrnehmungen, Sorgen und Hoffnungen austauschen konnten. Doch die amerikanische Plattform wurde schnell von China geblockt.

Umso erstaunlicher, dass nun auf einer Plattform aus der VR China chinesische Netizens den Austausch mit Taiwaner:innen suchen. Die App Xiaohongshu (siehe Infobox) ist in China besonders bei der jungen Generation sehr beliebt und auch in Taiwan zugänglich. Zwischen 2019 und 2022 mauserte sich die chinesische App neben Douyin (TikTok) zu einer der beliebten Apps in Taiwan.

Die Online-Plattform fokussiert sich auf das Teilen von Erfahrungen und Empfehlungen aus dem alltäglichen Leben. Laut Similar Web, einem Online-Analyse-Tool, machten Taiwaner:innen Mitte dieses Jahres rund 1,43 Prozent des Datenverkehrs auf der Plattform aus. Diese scheinbar kleine Zahl entspricht über 2,7 Millionen Nutzer:innen und damit mehr als 10 Prozent der taiwanischen Bevölkerung.

Xiaohongshu – The guide to your life (offizieller Slogan)

Gegründet: Juni 2013, Shanghai

Merkmal: Plattform für Online-Shopping und soziale Kontakte

Webseite: https://www.xiaohongshu.com/explore

Layout: Vergleichbar mit Pinterest, Funktionen ähneln jenen von Instagram

DAU (August 2023): 100 Millionen

MAU (Juni 2023): 190 Millionen

Nutzer:innen: Überwiegend junge Frauen der Generation Z (geboren nach 1990)

Hauptfunktion: Entdecken, Kreieren, Teilen, Suchen

Xiaohongshu (小红书: wörtlich „kleines rotes Buch“, eine Anspielung auf die Mao Bibel) ist eine Lifestyle-Plattform für junge Menschen, die 2013 in Shanghai gegründet wurde. Mit der Zielsetzung „Leben inspirieren, teilen und die Welt entdecken“ ermöglicht die App Nutzer:innen, ihren Lebensstil oder Interessen durch kurze Videos, Bilder und andere Formen der Interaktion zu teilen. Gute Empfehlungsalgorithmen und Nutzerfreundlichkeit haben zu wachsenden Nutzerzahlen beigetragen. Teil des Erfolgskonzeptes sind „Zhong Cao“ (种草) genannte Kaufempfehlungen in Livestreams, und das von Frauen geprägte Unternehmertum und Konsumverhalten auf der Plattform, oft als „She Economy“ (她经济) bezeichnet.

Nutzer:innen auf Xiaohongshu zeigen mehr Interesse für Taiwans Popkultur als Politik

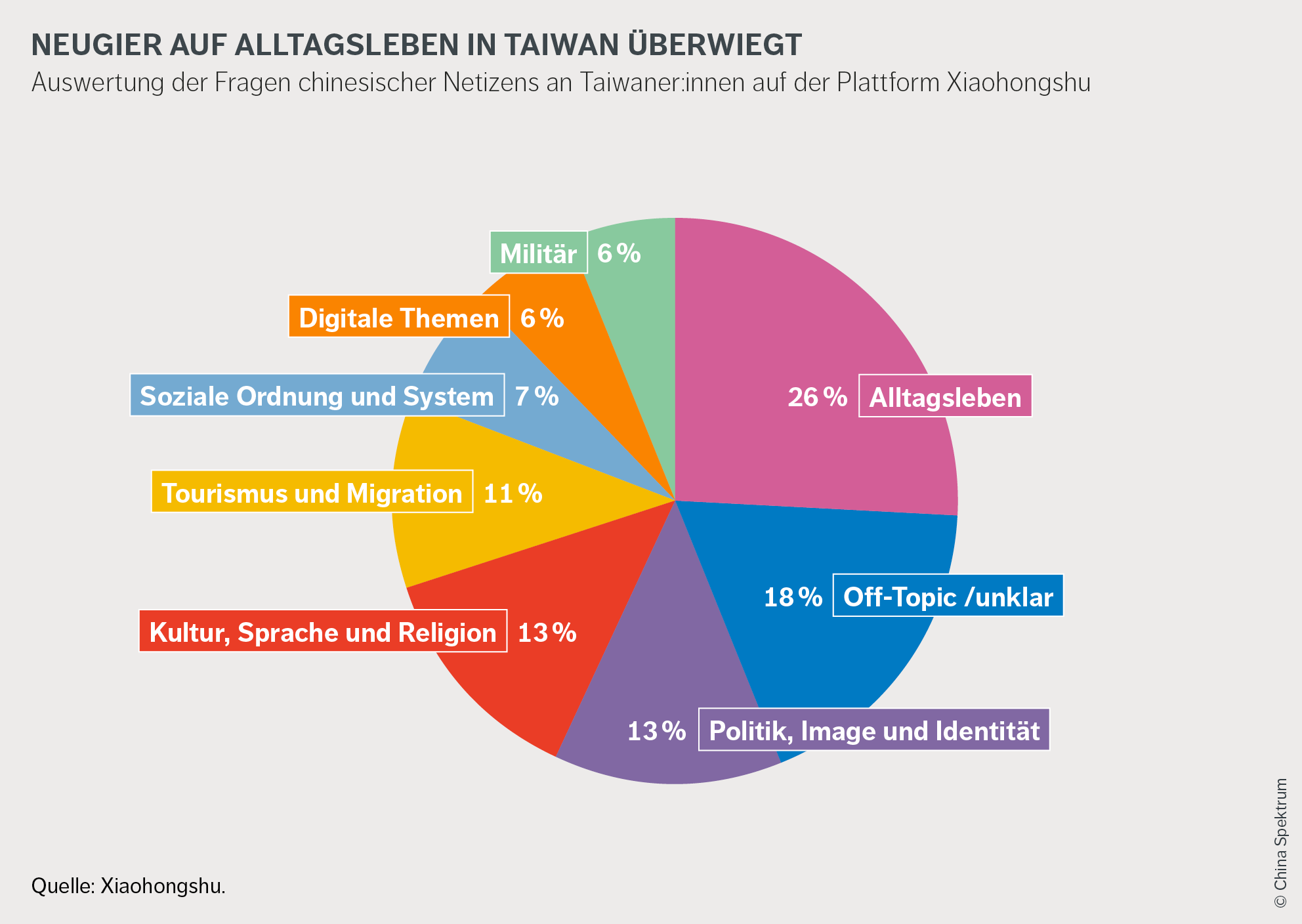

Welche Themen interessieren chinesische Netizens in Bezug auf Taiwaner:innen besonders? Wir haben dazu auf Xiaohongshu insgesamt 972 Fragen unter dem Hashtag „Festlandchines:innen stellen die Fragen und Taiwaner:innen antworten“ (大陆人提问台湾人回答) ausgewertet, die zwischen dem 7. Juli und 31. August 2023 veröffentlicht wurden. Teilweise haben taiwanische Netizens die Beiträge gelikt oder kommentiert.

Im Vordergrund steht der Austausch über das Alltagsleben in Taiwan (26%), z.B. zu Themen wie der Popkultur. Kritische Fragen zur Identität und dem Image Taiwans, die kontroverse politische Themen wie die politische Einstellung zur „Wiedervereinigung“ und militärische Themen berühren, werden ebenfalls gestellt (13%). Daneben finden sich auch neugierige Fragen zu Kultur, Sprache und Religion (13%). Generell offenbart sich in den Fragen viel Neugier, aber auch eine gewisse Zurückhaltung. So wünschen sich viele Chines:innen, nach Taiwan zu reisen (11%), doch einige fürchten sich vor Anfeindungen durch Unterstützer von Taiwans Unabhängigkeit.

Die am häufigsten gestellten Fragen beziehen sich auf das Alltagsleben und Taiwans Popkultur (26%).

„Sind chinesische Serien [in Taiwan] beliebt, bzw. was aus der Popkultur vom Festland ist in Taiwan am beliebtesten?“

陆剧流行吗,或者说大陆这边在台湾最著名的流行文化是什么?

Xiaohongshu 62049921, 1.8.2023

Auch wünschen sich viele Chines:innen, nach Taiwan zu reisen, fürchten sich jedoch vor Vorurteilen aufgrund der Spannungen zwischen China und Taiwan (11%).

„Würden Tourist:innen aus dem Festland von der ‚tai du‘ [Unterstützer der Unabhängigkeit Taiwans] ins Visier genommen? (Denn ich habe Videos gesehen, in denen td-Mitglieder den Reiseleiter angriffen haben.)“

大陆游客过去台湾旅游会被td针对吗(因为有看到过视频td分子当街撒泼针对旅游团导游)

Meitiandouhenkun, 17.7.2023

Unter den gesellschaftspolitischen Themen finden sich nicht nur Fragen zu Versicherungen oder dem alltäglichen Leben (6%). Xiaohongshu bietet auch Raum für – aus Sicht der Zensur sensible – LGBTQ-Themen.

„Ist ein Haus für Taiwaner:innen teuer? Wie hoch sind die Zinsen? Was tut ihr, wenn die gekaufte Wohnung nicht fertiggestellt wird? Gibt es Schulgebühren? Sind Krankenhausaufenthalte und Arztbesuche teuer?“

台湾同胞房子贵吗?贷款利率多少?期房烂尾怎么办的?孩子上学需要花钱吗?医院看病贵不贵?

Younigege, 31.7.2023

„Wäre es möglich, dass txl [Anm.: txl steht für „tongxinglian“, Homosexuelle] vom Festland nach Taiwan reisen, um eine Eheurkunde zu beantragen?“

大陆txl可以来台湾办结婚证吗?

Momo, 20.8.2023

Viele Chines:innen interessieren sich für die gemeinsame Geschichte sowie die taiwanische Kultur und Sprache, insbesondere die Verwendung der traditionellen Schriftzeichen (13%):

„Gibt es, abgesehen von der modernen Geschichte, irgendwelche Unterschiede zwischen den Schulbüchern Taiwans und des Festlandes in Bezug auf die alte Geschichte?“

抛开近现代历史,台湾和内地的古代史,课本上有没有什么区别?

Wys, 1.8.2023

„Schreiben die Taiwaner:innen sehr langsam? Das traditionelle Chinesisch hat doch viel zu viele Striche. [Lachendes Emoji mit Tränen]“

台湾人写字是不是很慢,繁体字笔画好多啊 [Lachendes Emoji mit Tränen]

Roumoqiezigaijiaofan, 8.7.2023

Obwohl Fragen nach den Lebenserfahrungen sowie Empfehlungen im Vordergrund stehen, ist auch die Politik und Identität Taiwans ein Thema (13%). Hierzu zählen auch einige wenige Kommentare zu militärischen Themen, die etwas nationalistische Töne anschlagen (1%).

„Darf ich mal fragen, wie ihr über das Thema Rückeroberung Taiwans denkt [Zwei lachende Emojis mit Tränen] ?“

请问你们怎么看待收复台湾这个问题 [Zwei lachende Emojis mit Tränen]

Chuanxuezidemao 1.8.2023

„Darf ich mal fragen, ob ihr wisst, wie weit ein Raketenwerfer vom Festland aus schießen kann?“

请问你们知道大陆火箭炮最远能打多远吗?

Xiaohongshu64590856, 26.8.2023

Xiaohongshu ist neben Douyin, der chinesischen Version von TikTok, eine der populärsten chinesischen Apps in Taiwan. Die Plattform wird in erster Linie von Frauen und Menschen mit höherem Bildungsniveau genutzt wird und zeichnet sich bislang durch einen respektvollen und interessierten Austausch der Nutzer:innen auf beiden Seiten der Taiwanstraße aus. Während die meisten festlandchinesische Nutzer:innen nach Taiwan fragen, sprechen manche über die „Provinz“ Taiwan (台湾省) und stützen damit den Gebietsanspruch der Volksrepublik China, der Taiwan als rechtmäßiges Gebiet betrachtet.

Gleichzeitig stellen chinesische Netizens auch immer wieder die Frage, wie man nach Taiwan einwandern könne. Der Begriff der „Unabhängigkeit Taiwans“ (tai du, 台独) und auch Diskussionen über LGBTQ-Themen unterliegen in China der Zensur. Netizens werden kreativ, indem sie Abkürzungen nutzen, um die Zensur zu umgehen. In den Kommentaren ist daher häufig nur ein „td“ (für tai du, Unabhängigkeit) oder auch „txl“ (für tongxinglian, Homosexuelle) zu lesen. Dass diese Themen einen Raum auf Xiaohongshu erhalten, liegt wahrscheinlich an der Vermarktung als unpolitische Plattform, auf der es um Alltagsleben und Popkultur geht und nicht um sensible politische Themen.

Im Vorfeld der Wahlen in Taiwan wird Xiaohongshu von beiden Seiten skeptisch beäugt

Die Analyse zeigt, dass die Fragen und Diskussionen von Netizens aus China und Taiwan auf Xiaohongshu primär um Alltagsthemen und konkrete Lebenskontexte kreisen und weniger um große, konfliktgeladene politische Fragen. Statt schroffer Forderungen nach einer gewaltsamen Eingliederung, wie man sie auf anderen Plattformen findet, steht hier ein interessierter Austausch zu Taiwans Kultur, insbesondere zur Popkultur und zum Tourismus, im Vordergrund. Doch auch Themen mit politischer Relevanz, wie Taiwans Legalisierung der gleichgeschlechtlichen Ehe im Jahr 2019, finden Raum.

Der Austausch auf Xiaohongshu ist zwar freundlich, aber die taiwanischen Behörden hegen Bedenken gegen eine mögliche Unterwanderung. Im Vorfeld der taiwanischen Präsidentschaftswahl im Januar 2024 ist mit hitzigen Debatten und weiteren Spannungen in den Beziehungen zu rechnen. Gerade der vermeintlich unpolitische, kommerzielle Charakter der App könne genutzt werden, um taiwanische Nutzer zu beeinflussen, mahnen mehrere taiwanische Forscher. So hat die taiwanische Regierung bereits im Dezember 2022 den Download und die Nutzung von Douyin (TikTok) für Geräte des öffentlichen Dienstes eingeschränkt.

Auch Chinas Regierung könnte den direkten Austausch auf Xiaohongshu irgendwann als für ihre politischen Ziele hinderlich empfinden, beispielsweise im Zuge einer nationalistischen Mobilisierung, und dann schnell unterbinden. Umso wertvoller ist die derzeitige Möglichkeit beider Seiten, sich relativ frei über ihr Leben und ihre Erfahrungen austauschen zu können.

Weiterführende Informationen:

Chinas Rolle in der Welt

Online-Länderranking - Stolz auf China, aber auch Bewunderung für die USA

Im September 2023 veröffentlichte der chinesische Staatsrat ein Weißbuch mit dem Titel „Eine globale Gemeinschaft der gemeinsamen Zukunft: Chinas Vorschläge und Maßnahmen“. Darin identifiziert Chinas Regierung zentrale Herausforderungen vieler Staaten wie Armut, Nahrungs- und Energiesicherheit, aber auch staatliche Verschuldung, gewaltsame Konflikte sowie die Klimakrise und ihre Auswirkungen und präsentiert Lösungsansätze für diese Probleme.

Das Weißbuch und die von China initiierte Serie globaler Initiativen sind Ausdruck des wachsenden Gestaltungsanspruchs der chinesischen Führung auf der globalen Bühne. Das spiegelt sich auch in der offiziellen Berichterstattung wider, die China als dominierende Weltmacht und den Westen als schwindenden Gegenspieler darstellt. Die Schlagzeilen vom Oktober 2023 zeigen dies sehr deutlich:

- Chinesische Errungenschaften und der führende Status des Landes werden regelmäßig hervorgehoben, sei es die Errichtung der weltweit größten Genbank für Ölpflanzen durch die Chinesische Akademie der Agrarwissenschaften, die neuesten Entwicklungen der weltweit längsten meeresüberquerenden Hochgeschwindigkeits-Eisenbahnbrücke in Zhejiang oder Wartungsarbeiten an der Umspannstation mit der weltweit höchsten Spannungsebene in Anhui.

- Auch Chinas zentrale Position in Asien und in der Welt werden immer wieder herausgestellt, beispielsweise die Veröffentlichung des neuesten Weltoffenheitsindex und Chinas Appell für globale Offenheit, die Eröffnung der China International Import Expo in Präsenzform und deren positives Signal für die Weltwirtschaft sowie die durch China forcierte engere Zusammenarbeit im ASEAN-Raum.

- Westliche Staaten ernten dagegen oft Kritik, wenn beispielsweise das Ende der „westlichen Hegemonie“ konstatiert wird, als Reaktion auf westliche, eher skeptische Berichterstattung über Themen wie Chinas Seidenstraßeninitiative oder auf einseitige Unterstützung des Westens sowohl im Russland-Ukraine- Krieg als auch im Israel-Palästina-Konflikt.

Doch inwiefern deckt sich diese offizielle Erzählung mit den Ansichten der chinesischen Bevölkerung, vor allem der jüngeren und weltgewandten Netzbüger:innen?

Netizens sehen China als "großartigstes" Land der Welt, begleitet von subtiler Kritik und Lob für westliche Staaten

Auf der chinesischen Frage-und-Antwort-Plattform Zhihu stellte der Nutzer Nihuerguizi (你乎二鬼子) am 17. April 2023 die Frage, welches Land das „großartigste“ der Welt sei (世界上称的上伟大的国家是哪个?). Die 2.000 Antworten auf diese Frage, die zwischen April und September 2023 gepostet wurden, haben wir uns genauer angesehen und daraus ein Länderranking erstellt.

Dass China für die Netizens auf Platz Eins steht, ist wenig überraschend. Dass die USA, Japan, Großbritannien und Frankreich direkt daran anschließen und sich auch Deutschland unter den Top 10 der „großartigsten“ Länder befindet, schon eher.

Das Ranking basiert auf unterschiedlichen Kriterien: die Häufigkeit der Erwähnungen, die Anzahl an positiven Bewertungen (Vote-ups) und die Stimmung (Sentiment) der Kommentare.4

Ein genauerer Blick auf die Antworten hilft, das Ranking besser einzuordnen:

- Meinungen über China umfassen neben ausgeprägtem Nationalstolz auch Kritik, die allerdings – der Zensur geschuldet – nur versteckt in Form von satirischen Übertreibungen und Andeutungen zum Ausdruck kommt. Zum Beispiel wird China mit Nordkorea, dem Iran und Russland zusammen als „großartig“ bezeichnet.

- Meinungen über andere asiatische Staaten rangieren von Bewunderung (zum Beispiel für Japans Wirtschaftserfolg) bis hin zu Ironie (zum Beispiel über Nordkoreas „göttliche“ Führung).

- Kommentare über westliche Länder wie Frankreich und das Vereinigte Königreich loben dagegen oft deren historische Beiträge zur Modernisierung und zur Demokratie.

- Italien und Indien werden für ihr reiches zivilisatorisches Erbe geschätzt.

China: Spitzenreiter – aber in zweifelhafter Gesellschaft

„Jedes Jahr, wenn die Taifune kommen, suchen unsere Parteikader in den Bergdörfern jeden älteren Menschen auf, damit niemand zurückbleibt [...] Ich glaube, China ist das großartigste Land.“

山村里每年要来台风了,党员挨家挨户去找老人[…] 我认为中国最伟大。

Zhesanye, 24.4.2023, 4.713 Likes

„Das großartigste Land der Welt ist die Volksrepublik China, gefolgt von vielen anderen großartigen Ländern wie Russland, Nordkorea, Iran, Syrien, Venezuela.“

世界上最伟大的国家就是中华人民共和国。其次伟大的国家包括以下诸多国家:俄罗 斯,朝鲜,伊朗,叙利亚,委瑞内拉等等。

Xinyu, 18.4.2023, 4.757 Likes

USA: Architekt der modernen Weltordnung und Motor der industriellen Revolutionen

„Seit Beginn des 20. Jahrhunderts haben die USA eine neue Weltordnung geschaffen, den Weltfrieden und die Demokratie gefördert und den globalen Handel vorangetrieben. Es ist die größte Nation der modernen Zeit.“

从20世纪开始,美国建立了新的世界秩序,推动世界和平与民主、推动全球贸易,是资本主义制度的集大成者.当今第一强国。

Mononoke, 21.4.2023, 589 Likes

Japan: Die Pioniermacht Asiens beim Wirtschaftsaufschwung

„In den 1990er Jahren hatte Japan bereits das dritthöchste Pro-Kopf-BIP der Welt.“

90年代日本的人均GDP已经是世界第三。

Sonder, 22.4.2023, 52 Likes

Vereinigtes Königreich: Pionier der parlamentarischen Demokratie und Rechtsstaatlichkeit

„Großbritannien war das erste Land, welches das Konzept einführte, dass ‚der König unter dem Gesetz steht‘ und ‚die Macht dem Gesetz unterworfen ist‘. Es war das erste Land, das eine parlamentarische Regierung einführte.“

英国:最先确立“王在法下”“权在法下”的国家。最先建立代议制政府的国家。

Senglutingyu, 1.5.2023, 524 Likes

Frankreich: Geburtsort moderner Menschenrechte und universeller Werte

„Die Französische Revolution hat erstmals das Konzept der angeborenen Menschenrechte und der Gleichheit vorgestellt […] Die universellen Werte der modernen Gesellschaft sind das Ergebnis der Französischen Revolution.“

法国大革命首次提出天赋人权,人人生而平等的观念 […] 这些现代社会普世价值观都是法国大革命的成果

Pengpai, 18.4.2023, 1.504 Likes

Nordkorea: Ein zynischer Blick auf Kim Jong-uns Führung

„Die bisherigen Führer sind quasi gottgleich. Besonders hervorzuheben ist der Mut, globale Großmächte […] mit einem Atomwaffenarsenal herauszufordern. […] Trotz Hungersnöten und schwacher Wirtschaft wurden diese großartigen Ergebnisse erzielt!“

历代领袖都[…]神武[…]手揣核武器,动辄就吓唬吓唬 […]一众世界强国,胆量上排世界前列 […] 甚至经常闹饥荒,在这种薄弱的经济下,还产生了上述的伟大成果[…]

Jingxiaoyoumenghan, 21.4.2023, 7.267 Likes

Russland: Schwindende Macht, aber reiches Kulturerbe

„Nach dem Zerfall der Sowjetunion […] hält sich Russland nur mit Mühe an der Spitze der großen Nationen. Jedoch sind die russische Kultur und Kunst erstklassig.“

解体后俄罗斯各方面下滑严重,勉强头部大国地位。但是俄罗斯文化艺术一流。

Nimingyonghu, 14.5.2023, 3 Likes

Deutschland: Bildungs- und Sozialsysteme werden positiv bewertet

„[...] Deutschland war Vorreiter beim Aufbau von Bildungs- und Sozialsystemen. [...] Nach der Wiedervereinigung wurden die Sozialleistungen in Ost- und Westdeutschland angeglichen [...] Deutschland bemüht sich kontinuierlich, den Bildungsstand und das Wohlstandsniveau seiner Bürger zu verbessern [...].“

[...]德意志首创各种教育和福利制度。[...]统一后没有对落后的东德地区搞区别对待, [...] 德意志一直想方设法提高国民素质和福利待遇 [...]

Zaoyuzheng, 20.4.2023, 30 Likes

Das Weltbild junger Menschen ist nicht so homogen wie die offizielle Linie vermuten lässt

Von außen entsteht mit Blick auf Chinas globale Ambitionen oft der Eindruck einer homogenen und immer nationalistischeren öffentlichen Meinung. Dies liegt einerseits daran, dass offizielle Kampagnen und die Berichterstattung der Staatsmedien zu Chinas Status und internationalen Geschehnissen durchaus die Wahrnehmung der breiten Gesellschaft beeinflussen. Dazu erschwert es die umfassende Zensur anderslautender Aussagen, die offiziellen Narrative in Frage stellen.

Das Streben Chinas nach einer neuen Weltordnung und seine wachsenden globalen Ambitionen stehen jedoch in einem gewissen Kontrast zur Stimmung innerhalb eines Teils der chinesischen Bevölkerung, insbesondere der gebildeten städtischen Mittelschicht. Auch wenn China und seine Führung nicht direkt kritisiert werden, stimmen die Netizens auf Zhihu zumindest nicht in die grundlegende Kritik Beijings an westlichen Ländern ein. Im Gegenteil, westliche Länder werden in Teilen durchaus sehr positiv besprochen. Weiterhin äußern Chines:innen auf verschiedenen Plattformen im Netz den Wunsch, aus China auswandern zu wollen, auch die Studierendenzahlen im Ausland steigen nach den Covid-Beschränkungen wieder.

Während die Partei- und Staatsführung nach innen Chinas Stärke und Überlegenheit demonstriert, droht sie möglicherweise die komplexen inneren Dynamiken aus den Augen zu verlieren. Hier scheint sich insbesondere eine Kluft zwischen der Regierung und einer gut gebildeten, jüngeren Generation, am Beispiel der Nutzergruppe auf Zhihu, aufzutun. Der Gegensatz zwischen offizieller Linie und individueller Meinung mag größer sein, als zu vermuten ist.

Weiterführende Informationen:

- Ge Zhaoguang: Die Windungen und Rückschläge im Weltverständnis traditioneller Chinesen

- LSE: China’s Political Worldview and Chinese Exceptionalism

- The Economist: China‘s latest attempt to rally the world against Western values

- Endnoten

-

1 | Bei der „Platform Economy“ handelt es sich um ein Geschäftsmodell, bei dem Unternehmen Online-Plattformen nutzen, um Verkäufer:innen und Käufer:innen zusammenzubringen.

2 | Zheng, Bingwen (2023): 为什么灵活就业人员会成为社会保险难以覆盖的“死角” (Warum flexible Beschäftigung eine „Sackgasse“ für den Sozialversicherungsschutz ist), CYOL, [online] https://web.archive.org/ web/20230830082709/https://m.cyol.com/gb/articles/2023-08/03/content_zxvZExSYZb.html [abgerufen am 30.10.2020]; Li, Mei (2022): 促进共同富裕背景下灵活就业人员参加社会保险的困境及对策 (Dilemmas und

Gegenmaßnahmen für flexible Beschäftigte in der Sozialversicherung im Rahmen der Förderung des Gemeinwohls), in: Journal of Beijing Federation of Trade Unions Cadre College, Bd. 2, Nr. S. 143, 26-32; Guo, Xiaoran (2023): 新业态下灵活就业人员社会养老保险参保现状研究 (Studie zur aktuellen Situation der Rentenversicherungsbeteiligung von flexibel Beschäftigten in neuen Betrieben), in: On the Way, S. 263-266; Chen, Jian (2023): 启东市养老保险征缴现状及前景的研究 (Eine Studie über die gegenwärtige Situation und die Aussichten der Rentenversicherung in der Stadt Qidong), S. 128-130; Cui, Ruixia (2023): 推进企业职工基本养老保险参保扩面工作的探讨 (Diskussion über die Förderung der Ausweitung der Teilnahme an der Basisrentenversicherung von Unternehmensmitarbeitern), S. 41-44; Tan, Jinke und Yanxing Luo (2023): 新业态灵活就业人员基本养老保险制度优化研究 (Studie zur Optimierung der Basisrentenversicherung für flexible Beschäftigte in neuen Betrieben), in: 新业态灵活就业人员基本养老保险制 度优化研究 (Studie zur Optimierung der Basisrentenversicherung für flexible Beschäftigte in neuen Betrieben), S. 17-26; Li, Jinyu (2021): 新业态灵活就业人员养老保险问题研究 (Studie über die Rentenversicherungsprobleme flexibler Arbeitnehmer in neuen Unternehmen), S. 158-160; Zang, Limei (2021): 灵活就业人员养老保险问题及应对措施 (Probleme der Rentenversicherung für flexibel Beschäftigte und Maßnahmen zu deren Bewältigung), S. 16-19.3 | Zudem fällt auf, dass strukturelle Probleme auf staatlicher Seite häufiger von Universitäten aufgezeigt werden. Wissenschaftliche Mitarbeiter bei Sozialämtern heben eher die individuelle Ebene hervor, was einerseits durch die direkte Erfahrung und andererseits mit dem Abwehren von Verantwortung zusammenhängen mag.

4 | Gegenstand der Analyse waren 2000 zwischen April und September 2023 gepostete, Länder-bezogene Antworten auf die oben genannte Frage. Mittels Natural Language Processing wurde jedem Kommentar ein positives oder negatives Sentiment zugewiesen. Diese Bewertungen wurden anhand der Anzahl der „Vote-ups“ gewichtet und dann auf Länderebene zusammengefasst.

Author(s)

Head of Program

Senior Associate Fellow

Former Analyst

Author(s)

Head of Program

Senior Associate Fellow

Former Analyst