picture alliance / ASSOCIATED PRESS | Jose Luis Magana

Tracker

China Global Competition Tracker

China’s global debt holdings are increasingly a liability for Beijing

No. 2, July 2023

What you need to know

China’s global debt holdings are increasingly a liability for Beijing

Just as China’s economic recovery has proven lackluster, so too has much of China’s economic engagement with the rest of world sputtered along in Q2 of 2023. In this edition of the MERICS China Global Competition Tracker, our experts look into three different issues that reflect Beijing’s struggle on the international stage, some of its successes, and the challenges and opportunities facing some of its national champions as they look overseas for future growth.

In our top story, MERICS Analysts Francesca Ghiretti and François Chimits look into China’s now massive role in developing country debt holding at a critical moment. As developing countries emerge from the pandemic with massive debt burdens, an international effort by creditors to restructure debt for the worst affected countries, and to write off some of the burden, stalled because of Beijing’s inaction. As our experts indicate, China is the linchpin of the issue, and the longer that it holds back progress on debt relief/restructuring talks, the greater the risks become for the debtor countries, the lending countries, and the global economy as a whole. What Beijing does next could have massive real-world implications for many, but most of all for China’s reputation, let alone its own financial stability.

Meanwhile, our regional spotlight covered by MERICS Analyst Aya Adachi examines China’s activities in Georgia. The country has surged in its importance for many key infrastructure projects related to the ‘middle corridor’, a transportation route that stays on the south side of Russia – which has become more viable in a post-Russian-invasion world. While concerns abound regarding fairness and corruption for projects in the country in general, it is also the case that many of the projects that China’s own companies are leading on are not connected to the BRI, but are instead financed by mulit-lateral development banks. The situation is further complicated by Georgia’s status as an EU member state candidate, as critical infrastructure projects built and often managed by Chinese SOEs could someday be absorbed into the EU if Georgia can accede.

Finally, MERICS Senior Analyst Jacob Gunter covers China’s main nuclear energy companies in his Key Players segment. Having spent decades trying to catch up to European, Russian, and North American nuclear energy technology, China’s own nuclear champions are attempting to cement themselves overseas. However, these players are facing limitations abroad, in part due to the sheer demand for nuclear reactors in their home market (which sucks up much of the supply that China’s companies can fulfil), but their domestically developed Hualong One reactor design has yet to build up a track record to compete with long-established competitors’ designs. Instead of an immediate source of competition to European industry, like in the EV sector, the nuclear energy sector represents a medium to long term competition risk to European players. However, even then, China’s nuclear energy champions will be competing with a growing array of renewable and green energy types, so their success in capturing global nuclear market share is far from certain.

Top Story

Will China stall new plurilateral debt rescheduling or gain status in a new international framework?

Many developing economies have been pitched into dire financial circumstances by the toxic mix of the Covid-pandemic, high prices for food and commodities, a stronger US dollar and heightened financial uncertainties. In the last three years, there have been as many sovereign defaults as in the previous decade, which already had a substantial number of default in the aftermath of the global financial crisis . These simultaneous crises have reactivated international discussions among creditors on how to develop a coordinated approach to international debt rescheduling. Amid the pandemic, the G20 and official lenders groups (the Paris Club) launched the Debt Service Suspension Initiative (DSSI) at first, and later the Common framework in 2020 to provide more structural debt relief in close coordination with IMF programs.

The novel feature of these debt rescheduling negotiations is that a “developing economy” – China – is a participant on the lender-side. China is not just a creditor. In most cases it is the largest creditor. And, true to its revisionist approach to the international economic order, Beijing has its unique approach to international lending and debt restructuring. For international development lending, it favors higher rates, has higher appetite for risk, less transparency and bigger loans. Its debt restructuring is also uniquely opaque and bilateral. The world of official lending has its faults, but past crises have pushed traditional lenders to establish some constraints, especially some transparency, for loans and restructuring, to avoid chaotic, standalone restructurings.

The biggest external risk to China’s economy is a novel one

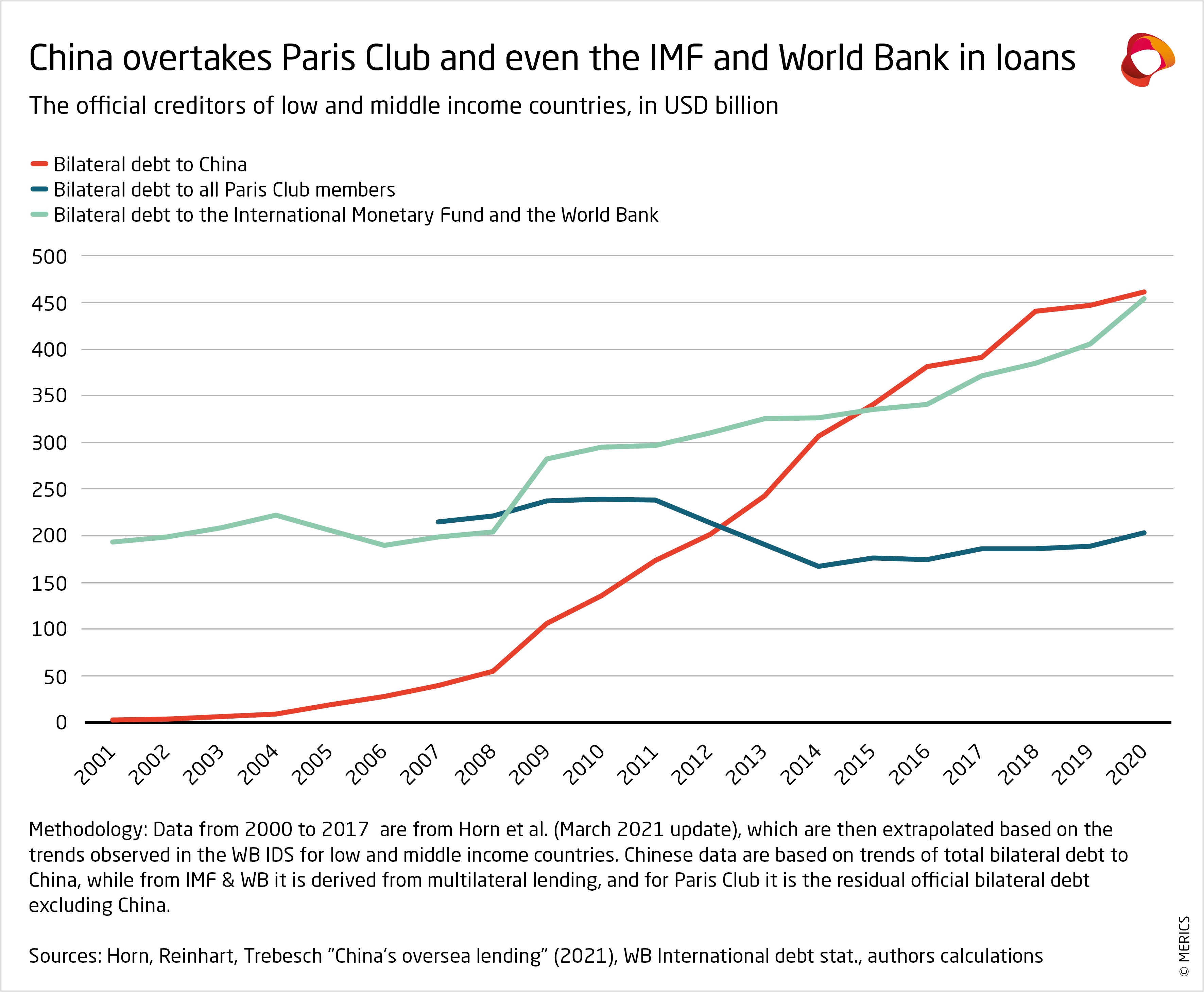

In a decade, the People’s Republic of China (PRC) has become the major bilateral lender to developing countries (which with market-debt, mostly bonds on foreign markets, makes up for the external debt of countries). China went from being marginal actor to the number one official creditor, investing USD 450 billion in net lending (see exhibit).

Now, 60 percent of this funding is at risk of default. An extreme scenario of total financial meltdown in emerging economies would put those official loans at risk. Certainly, there would also be a substantial hit to the roughly USD 200 billion of net paid-in development financing that Beijing has provided to developing countries as well as the USD 843 billion of Chinese direct investment in developing economies. For Beijing, somewhere around USD 1.5 trillion of assets could be at risk. Although this scenario is unrealistically extreme, it illustrates why a leading Chinese economist, Cao Yuanzheng (曹远征), has characterized the developing economies’ debt difficulties of as “the biggest external risk to the Chinese economy”.

Beijing lends at higher interest rates than most development finance loans

Chinese lending is remarkable not only for its scale, but also for the longer payment period for the principal, longer grace period and larger volumes. Interest rates are closer to market rates (i.e. 5 percent and above) than the preferential rates typical of traditional development financing (around 2 percent). Perhaps most importantly, Chinese loans are also abnormally opaque, which explains the significant variations in the estimates already given. As China is not a member of the Paris Club or the OECD, it has no obligation to publish the numbers. Furthermore, the blurred line between China’s public and private spheres (particularly opaque in the financial sector) makes it hard to distinguish between commercial and official lending. In Zambia, Ethiopia and Ghana, the total amount of Chinese loans that needs to be considered within their official restructuring would be doubled if loans from China’s state-owned commercial banks backed by official export insurance (Sinosure) were counted, in line with “Paris Club” standards.

Besides, most Chinese financing comes with uniquely tight non-disclosure obligations and explicit exclusion-clauses from coordinated debt-relief initiatives.

After 2017, the sudden decrease in new Chinese funds, which had made up a very substantial source of external financing, amplified the external shocks for low income countries. Countries that were heavily reliant on major Chinese investment are particularly prone to financial difficulties since then. In fact, in the past decade Beijing has already conducted more than 75 percent of international “credit events” (default and debt restructuring).

Chinese financing is part of Beijing’s narrative that it champions developing countries

China has a strong preference for bilateral and opaque management of default and restructuring. Re-negotiations are also characterized by a preference for debt-deferrals over write-offs, and the over-hyped risk of asset seizures remains extremely rare in practice. Even if the most extreme version of the “Belt and Road debt trap” theory is not backed by facts, it is true that such a concentration of external debt creates serious concerns about the degree of agency that debtor countries possess in dealing with China, especially given the opacity around loans and Beijing’s tendency to leverage economic dependencies.

Internationally, the PRC has long positioned itself as the champion of developing economies, an argument that stands at the core of its domestic legitimating narrative. And to anyone who might see a tension with China’s own high speed development, the party’s media mouthpiece recently stated, “China will always be a developing country”. This narrative is now being stress tested by China’s role as the leading creditor in a wave of defaults by developing economies.

Zambia, Sri Lanka, Ethiopia, Ghana, Ecuador, Chad and Suriname have already formally defaulted: Chinese loans account for more than 60 percent of their official external debt. Chinese finance has a similar footprint in many countries – Pakistan, Afghanistan, Sudan, Maldives, Argentina, Kenya – where the financial situation is not much rosier.

Beijing’s stance is causing debt restructuring negotiations to stall

China first participation in a plurilateral effort on international debt was initially quite a success, with 65 percent of the deferred payments (under the DSSI), while representing only 25 percent of the due payments over the period. The discussions defined – in an initial way, at least – who is a Chinese “official bilateral creditor” and included most lending by Chinese policy banks. (There is no agreed international definition of official bilateral creditors.)

Discussions on debt restructuring, under the Common framework, ran into trouble around the extent of Chinese debt to be submitted to debt restructuring so an IMF program could be initiated. Things got worse when Beijing added an unusual demand, creating unprecedented delays for such discussions.

When outright defaults emerged, China and the Paris Club opened a formal communication channel with the IMF potential bail-out programs. The programs are conditional on all major bilateral lenders restructuring external debt towards a sustainable path, under a soft standard established by the Paris club on the principle of the “comparability of treatment” among creditors (i.e. similar treatment of all official debt, irrespective of the identity of the issuer/holder). It means official lenders must accept a cost for setting the debtor back on sound financial tracks. The debtor commits to some structural reforms to prevent another debt pile up, before the IMF agrees to pour in more resources.

The cases of Zambia and Sri Lanka, the first two major debtors for which IMF programs were ready, unfortunately did not go as smoothly as the opening DSSI round had, so they could not access IMF bail-out programs. After months of negotiation and high-level pressure, Beijing has yet to formally accept the inclusion of its policy bank loans in the restructuring effort.

On top of this, China also awkwardly demanded that loans from multilateral development banks (MDBs, such as the World Bank) be included in the official restructuring. This demand runs counter long-standing practices that exclude MDB financing from restructuring in order to make debt repayment and restructuring more stable. The IMF/WB Spring Meetings in April revived hopes of a functional structural solution, but so far nothing has yet been confirmed.

In summary, for the IMF to intervene and get struggling recipient countries back on a sustainable path, it requires bilateral lenders like China to write down a significant portion of their debt holdings. However, China has so far refused to do for the all its bilateral credit and demand that the MDBs commit to writing down their debt holdings as well – which is not an equal move since MDBs issue loans at far lower rates than China’s banks have. If that happened, China's banks with their higher rates would then recover far more of their losses than the MDBs with their lower rates would – an obvious issue for MDBs.

China’s goals are unclear but the implications of dragging out negotiations are bleak

China’s challenging stance in the restructuring discussions, coupled with a lack of clear communication, has left partners and analysts guessing at the reasons behind China’s positions. Some see genuine policy mismanagement while others see opportunistic delays to minimize direct financial costs.

Policy mismanagement is plausible reason, given the complex domestic political and administrative structures for such discussions. The People’s Bank of China (PBOC) holds the seat at IMF discussions, the Minister of Finance (MoF) holds the one in the G20 body supervising the DSSI and the Common framework. Moreover, the large state-owned banks, especially the policy banks, like China Development Bank (CDB) and the Export Import Bank of China (Exim) are owned by a web of institutional entities, mostly with the PBOC and the MoF as final owners. The head of those powerful institutions often has a high political standing, sometimes outranking their regulators. The result is a conflicted relationship with their regulators.

The PRC’s still immature domestic framework on debt write-off is another plausible factor. Standard regulations to smooth debt write-off are a recent development. Unlike OECD countries, China has no specific regulation on foreign debt write-off.

On the top of all this, debt forgiveness to developing economies is a topic that gets a rather negative reception from domestic audiences uncomfortable with aid to “poor” foreigners while poverty remains at home. With China Exim holding the chair for China in both the DSSI and the Common Framework, it is possible that China’s position overly represents its banks’ reluctance to take losses. Internal disagreements were acknowledged by the head of the PBOC international department in a recent webinar. The PBoC governor said in December that “for overseas claims, in accordance with the principle of ‘who invests bears the risk, and who makes the decision is responsible for risk compensation’, financial institutions and enterprises bear the main responsibility”. As the PBoC’s swap lines seem to have been extensively mobilized to bail-out international “commercial” loans by Chinese banks, it seems likely banks are trying to avoid losses because they have already taken a hit.

Or Beijing may be deploying opportunistic arguments to minimize its financial losses. The Suriname case, where an escrow account was hidden from the IMF and continued making some interest payments to Exim (in breach of the pause agreed on by creditors) has fueled this hypothesis. Recent findings that China used its official swap lines (usually excluded from restructuring) to bail out some loans by Chinese banks, also fed mistrust.

The final resolution of those cases will say a lot of Beijing’s preferences on the international economic order

On the 22nd of June, the IMF and the main creditors announced to have secured a three-year-in-the-making agreement on the restructuring of the Zambia’s bilateral international debt . Surely good news, the details had not been made public at the time of writing and no formal agreement had been signed yet. If Beijing has dropped its unusual demands on the treatment of MDBs, it seems likely that the amount of debt finally restructured will be lower (by ~20 percent) than previously estimated. Given China’s holdings made up 60 percent of Zambia’s total debt, the lower number likely indicates that Beijing has been able to exclude at least some of its credits from the more stringent agreement on the official lending. This exclusion dents the previously established soft-standard of including all State-guaranteed bilateral debt, and it indicates further troubles down the road to establish a clear set of standards for international debt restructuring.

If Beijing keeps delaying, it will undermine its reputation in the EU and globally

The lack of positive engagement from Beijing risks seriously degrading China’s international image in both advanced and developing economies. The longer the IMF programs are put on hold, the harder the impacts on local populations further down the road.

Europeans should give their Chinese counterparts a clear message about the importance of a plurilateral and transparent framework to deal with international debt restructuring, especially at high level. A positive move from Beijing would provide a focus for positive cooperation for the greater good, bolstering the possibility of considering Beijing as partner. If there are no positive results, Beijing will be seen more as a systemic rival. Either way, the outcome of such approaches would be a helpful input for European thinking on how and why to engage China.

By facilitating international restructuring and preventing the weaponization of already difficult negotiations, such a framework would benefit the greater good, and developing countries in particular. At a time of heightened geopolitical tensions, such cooperation would likely generate positive spillovers.

Regional spotlight

Georgia showcases China’s growing competitiveness in winning projects financed by others

The Middle Corridor from China to Europe through Kazakhstan, Azerbaijan, Georgia and Turkey could provide an alternative route for Chinese goods to reach Europe without passing through Russia. Since President Vladimir Putin’s invasion of Ukraine, the EU and European companies have been reinvigorating their policies towards the South Caucasus and Central Asia and are now pushing for the expansion of the “Middle Corridor”.

Georgia’s government manages its strategic position carefully by engaging with multiple players to balance its vulnerable location on Russia's border. China and Chinese companies have risen as prominent actors through investments, Belt and Road Initiative (BRI) projects and also as contractors building infrastructure projects funded by others.

Georgia's strategic position draws interest from China and Europe

Today, Georgia is trying to revive its economy by leveraging its geographic position between Europe and Asia, Russia and the Middle East to become a global trade and manufacturing hub, re-enacting a modern version of its historical role serving the original ‘Silk Road’ and Black Sea ports.

Georgia has gained plaudits for creating a smooth business environment. In 2007, the World Bank named Georgia “the number one economic reformer in the world”. Between 2007 to 2008, Georgia’s ranking for ease of doing business rose from 112 to 18. By 2020, Georgia had climbed to seventh place. To attract investors and lenders, the government has hosted the Silk Road Forum and made Georgia the most active country in the Caucasus region in signing Free Trade Agreements with major players, namely, EU, China, Turkey, and the Hong Kong Special Administrative Region.

In contrast to nearby countries, Georgia has been pro EU and pro-US, as seen in its eagerness to join the EU, its involvement in Iraq War and in the US-led mission in Afghanistan. However, Georgia must reckon with Russia’s strong regional influence and a Russian occupation in some of its territory; this has limited its room to maneuver with neighboring countries and ability to promote the Middle Corridor. To counter Russian influence, Georgia has increasingly turned to China to supplement its engagement with the EU and United States.

China Inc has been busy in Georgia, often in internationally financed, non-BRI projects

In the past eight years, Georgia-China relations gained have pace: in 2015, the privately-owned Hualing Group made the biggest Chinese investment in Georgia to date; Georgia joined BRI in 2016; and swiftly agreed a bilateral FTA in 2017, the region’s first. China-Georgia trade volumes rose from USD 362.2 million to USD 1.9 billion between 2010 and 2022. In the same period, China’s share of Georgia’s total imports rose from 6 percent to 8 percent, while its share of total exports rose from 2 percent to 13 percent. It is now among Georgia’s top three trade partners, after Turkey and Russia.

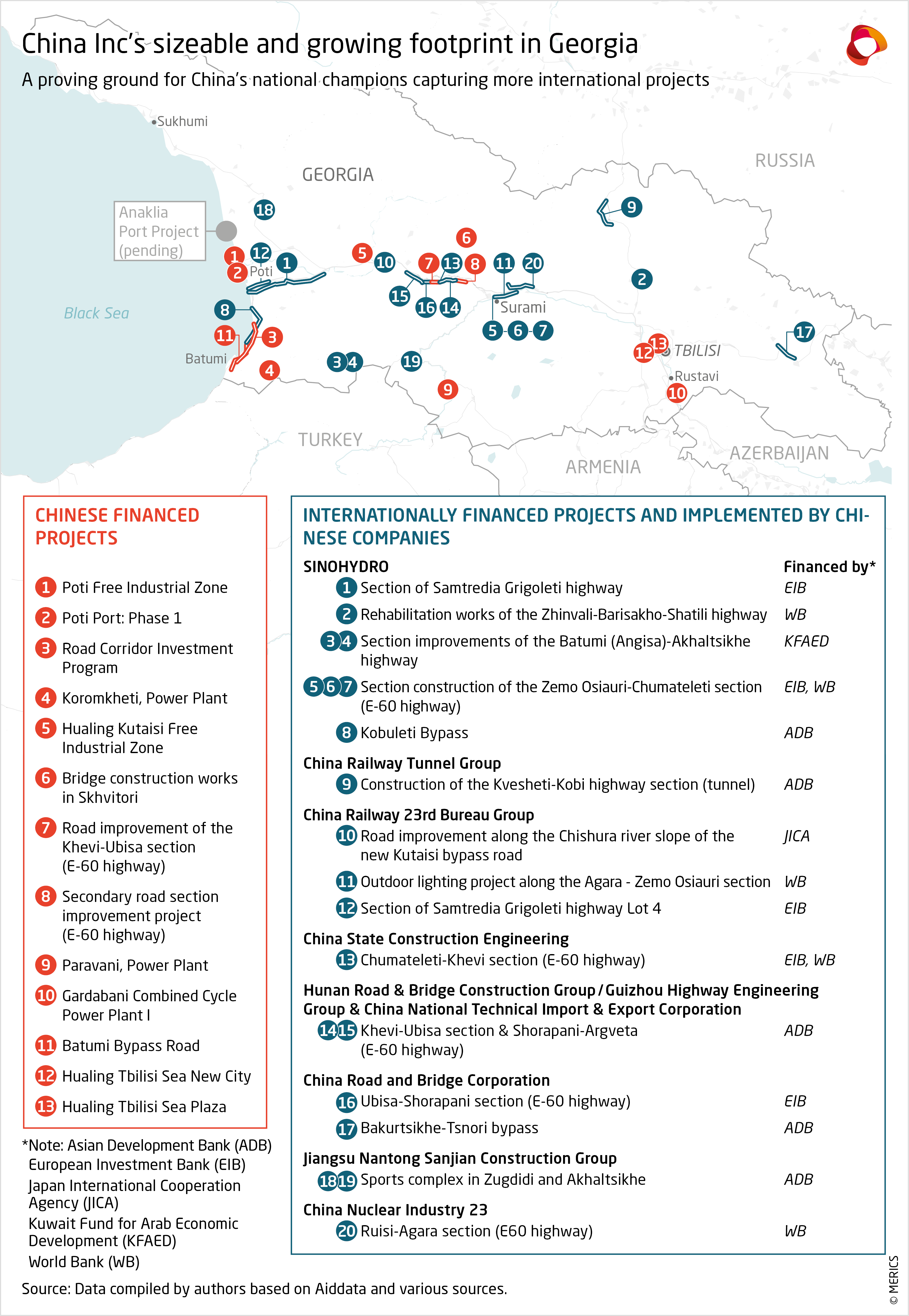

China has helped finance 13 projects in Georgia (see map), such as roads and powerplants and two strategically located zones. The Poti Free Industrial Zone is a manufacturing base near Poti Port on the eastern Black Sea, which has been 75 percent owned by CEFC (Euro-Asian) LLC China, a subsidiary of China’s giant private firm, CEFC Energy since 2017. The United Arab Emirates’ Ras Al Khaimah’s owns 15 percent and Georgia 10 percent. Hualing Free Industry Zone in Kutaisi is under the direction of Hualing Group, which took the management of the new zone in 2015 for 30 years with plans to invest USD 30 million over time. The zone is seen as a connecting hub between Kutaisi International Airport, Poti port and the capital city, Tbilisi.

Georgia has received fewer Chinese development finance projects than some Middle Corridor countries (Azerbaijan and Turkey) though significantly more than Armenia. Despite Georgia’s appeal as a potential economic hub, it has not been a BRI priority.

China’s presence in Georgia owes much to its companies than to Beijing’s development finance

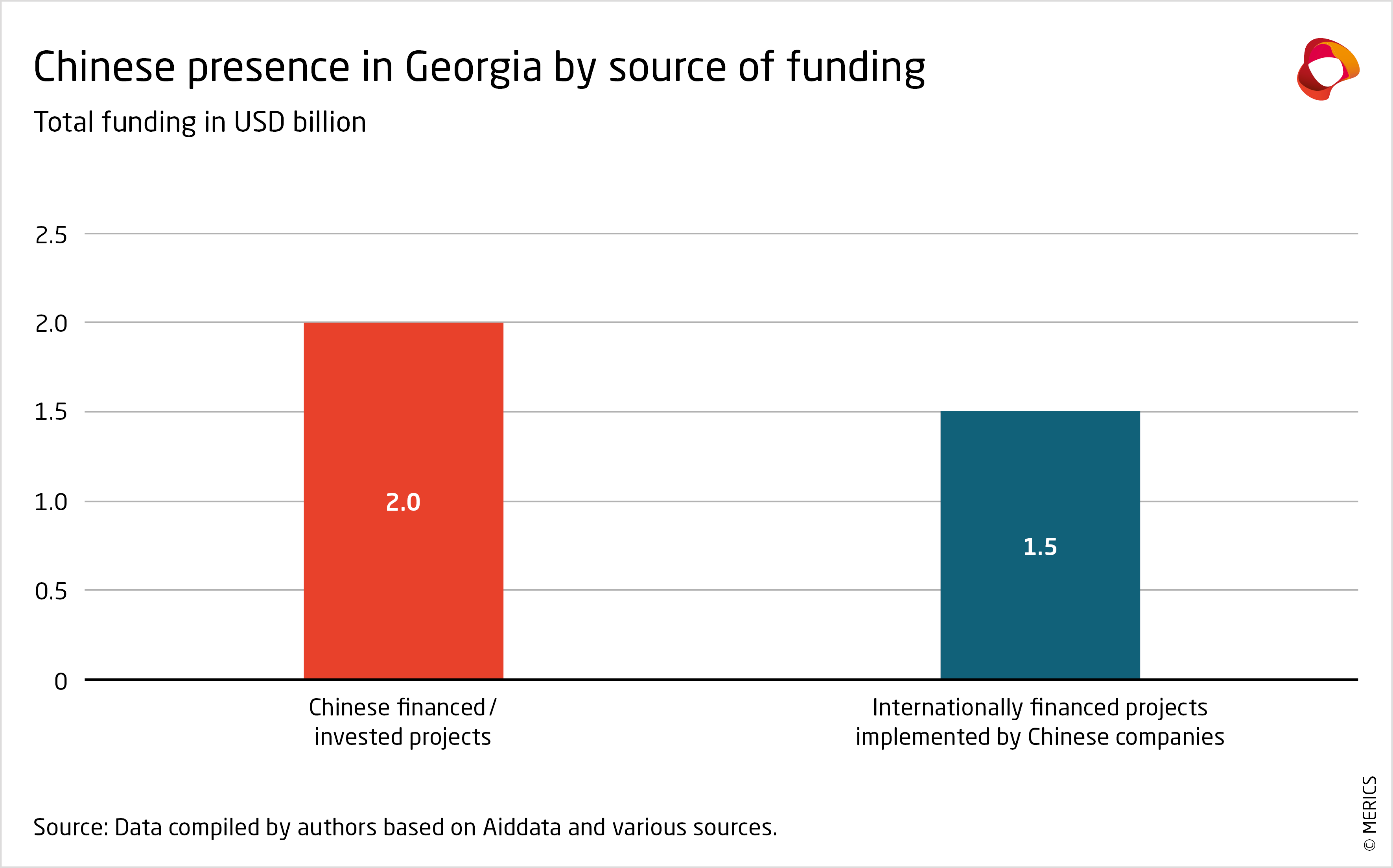

Chinese companies have won tenders on 20 infrastructure projects funded by international financial institutions (IFIs), including the European Investment Bank (EIB), World Bank and Asian Development Bank (ADB). The sheer number of such deals in Georgia is striking, although such contracts exist elsewhere (e.g., Croatia’s Pelješac Bridge and the Solomon Islands port project). In Georgia, Chinese companies are involved in deals worth a total of USD 3.5 billion, of which 43 percent are financed through credits provided by IFIs to the Georgian government and the rest is Chinese funded (see exhibit).

Georgia’s Ministry of Infrastructure has said Chinese firms have done well because European companies “are mostly unable to compete with large Chinese companies in terms of qualification and price” as well as “experience”. But some Chinese companies that won tenders managed by the Georgian government have a record of mismanaged projects and corruption or ended up on international blacklists by IFIs, including WB, African Development Bank, International Monetary Fund.

Overall, China Inc has thus far met few hurdles to operating in Georgia where it is met by weak state institutions and private interests significantly influencing decision-making processes, which has been termed “state capture”. Observers have pointed out that Georgian authorities have exhibited a striking disregard for due diligence measures in their dealings with China, even in even in sensitive industries.

Obstacles for Georgia and the ‘middle corridor’

Despite being the shortest route between western China and Europe, many logistical barriers stand in the way of the Middle corridor becoming a success. First, trade movements take longer due to the transshipments from train to ships at the Caspian and Black Sea. Transits through multiple small countries that have yet to synchronize and harmonize their import and export procedures add to difficulties.

Second, regional instability in the South Caucasus and Georgia’s own problems can discourage investments and slow progress. The ongoing conflict between Armenia and Azerbaijan, Russian occupation of Georgian territory and instability in Afghanistan are all sources of volatility. The conflict between Georgia’s neighbors and their allies – Armenia backed by Iran and Russia is set against Azerbaijan supported by Turkey and Israel – remains deadlocked, despite US and EU mediation attempts in May 2023.

Finally, prospects for the success of the Middle Corridor depend on whether the stalled Anaklia Port Project can be brought to life. Considered the only location for a new deep seaport on the eastern Black Sea, it could be a game-changer by increasing trade capacity to create a viable route. Plans from a US-Georgian consortium remain stalled due to pressure on Georgian elites from Russian interests objecting that a deep sea port could host NATO ships and compete with Novorossiysk port in southern Russia.

Using the window of opportunity to redesign the middle corridor route

Obstacles remain significant. But diversifying trade routes away from Russia is now of strong interest to corporates and to regional and external government stakeholders. Georgia and neighboring states have ramped up inter-state cooperation since Russia’s assault on Ukraine and signed memorandums on railway cooperation and trade facilitation. In March 2022, Georgia, Azerbaijan, Turkey and Kazakhstan produced a quadrilateral statement on the need to develop the Trans-Caspian International Transport Corridor (TCITC), also known as the Middle Corridor.

European rail and shipping companies have swiftly put their Middle Corridor services in motion. The Netherland’s Rail Bridge Cargo, Danish shipping corporation Maersk, Finland’s Nurminen Logistics, Georgia’s state railway company and a joint effort by Austrian OBB Rail Cargo Group and Dutch Cabooter Group all started services between China and Europe via the Middle Corridor – some within weeks after Russia’s attack on Ukraine.

The results are visible: cargo shipments along the Middle Corridor swelled tenfold from 350,000 metric tons and 530,000 in 2020 and 2021 to 3.2 million metric tons in 2022. But the middle route’s overall capacity remains low compared to the northern route via Russia’s Trans-Siberian railway, which moved 144 metric million tons of cargo in 2020. The southern sea route from China is projected to carry more than one billion metric tons in 2023. However, the rapid increase in Middle Corridor trade shows its potential, despite low overall tonnage.

Implications for Europe

Since Russia’s invasion of Ukraine, Beijing does not appear to have changed its approach to the South Caucasus. Beijing’s recent announcement that construction would start on the China-Kyrgyzstan-Uzbekistan railway indicates China continues to prioritize Central Asia. While Beijing chooses to focus on the eastern sections of the Middle Corridor, Europe appears to be closing in on its commitment in the South Caucasus.

The EU has a pressing interest in engagement and stability in the South Caucasus. In 2022, it gave Georgia a roadmap of reforms needed to gain EU candidate status, and it is trying to mediate between Azerbaijan and Armenia. Specific moves to enhance the Middle Corridor include a planned undersea cable to improve connectivity to Georgia and reduce dependence on lines through Russia, amid concerns about global data infrastructure.

However, the EU has struggled to improve cooperation with Georgia, which has preferred working with Chinese companies that have been enabling partners for corruption. For Georgia’s government, China is a key actor, as long as Beijing remains ambiguous on Russia and offers economic opportunities. Opinion polls in Georgia show neutral public attitudes towards Chinese investment overall. This could quickly change if Beijing were to increase its support for Moscow, as anything that bolsters Russian power is a red line for Georgians. For Beijing, the question is whether it has enough leverage over Moscow to make Russia accept growing Chinese influence in the region without fully supporting Russia’s position in the South Caucasus. The EU and European companies looking into recalibrate their positions in Georgia should use opportunities to challenge of potential changing perception of China linked to its ambiguous dynamic with Russia.

Key Player

China’s nuclear energy champions are only slowly turning their focus overseas

China arrived relatively late to the nuclear energy game. It relied on Soviet technological support in the 1950s, so its nuclear industry was disrupted by the Sino-Soviet split. It made progress in the 1960’s, notably testing its first nuclear bomb, until the Cultural Revolution caused more setbacks. With reform and opening up, China renewed its drive to catch up in nuclear technology, including for energy generation. China’s two main nuclear power champions are:

- China National Nuclear Corporation (CNNC), which emerged from the Ministry of Nuclear Industry and has always been a Beijing-based state-owned enterprise (SOE) under the State-owned Assets Supervision and Administration Commision (SASAC) which reports to the State Council.

- China General Nuclear (CGN), which began as a locally owned SOE in Guangdong before expanding nationally and eventually being reassigned to SASAC.

The duo were tasked with catching up with foreign nuclear energy technology though they have also been in a race with one another. Both firms partnered with foreign nuclear energy firms to develop first and then second generation nuclear tech. As they approached third generation tech, they were ordered by Beijing to merge their designs, producing the Hualong One third generation reactor design. Although many of the reactors under construction in China and overseas use other designs, Beijing’s ambition is that Hualong One (and eventually the Hualong Two) should become the primary design for China-produced reactors.

In China itself, Hualong One reactors are currently three of the 55 reactors in operation; 10 of the 23 under construction; and 21 of the 45 in planning. Overseas, the Hualong One has had limited take up so far, with a mere two reactors under construction in Pakistan and a third planned in Argentina. However, according to the World Nuclear Association, China has signed MOUs, entered into discussion with, or prepared bids for Hualong One reactors in the UK, Egypt and Kenya. It has pursued business with other reactor designs in Iran, Turkey, South Africa, Sudan, Armenia, and Kazakhstan.

CNNC and CGNs ambitions are complicated by US restrictions, both domestically and overseas. Both companies are on a variety of blacklists that restrict access to US technology, including through the Entities List, which covers CGN, and some of CNNC’s subsidiaries. The United States classes both companies as directly supporting China’s military, most explicitly through Executive Order 13959 which “prohibits investment by US persons in ‘ostensibly private and civilian’ companies that directly support the PRC’s military, intelligence, and security apparatuses.” This limits CGN and CNNC’s access to the US market and technologies, and adds an extra geopolitical consideration for countries thinking of partnerships with either firm.

China Inc.’s nuclear firms remain busy at home for now

China’s nuclear energy duo’s overseas footprint is limited compared to that of its most globally active SOEs. The number of nuclear plants built by CNNC and CNG overseas is tiny compared to those developed by Russia, France, the UK and the United States. However, given their late start, it is impressive in relative terms. Yet, looking at the number of planned projects outside China being led by CNNC and CNG over the next 10-15 years, they lag far behind other sectors of China Inc.

This is primarily due to:

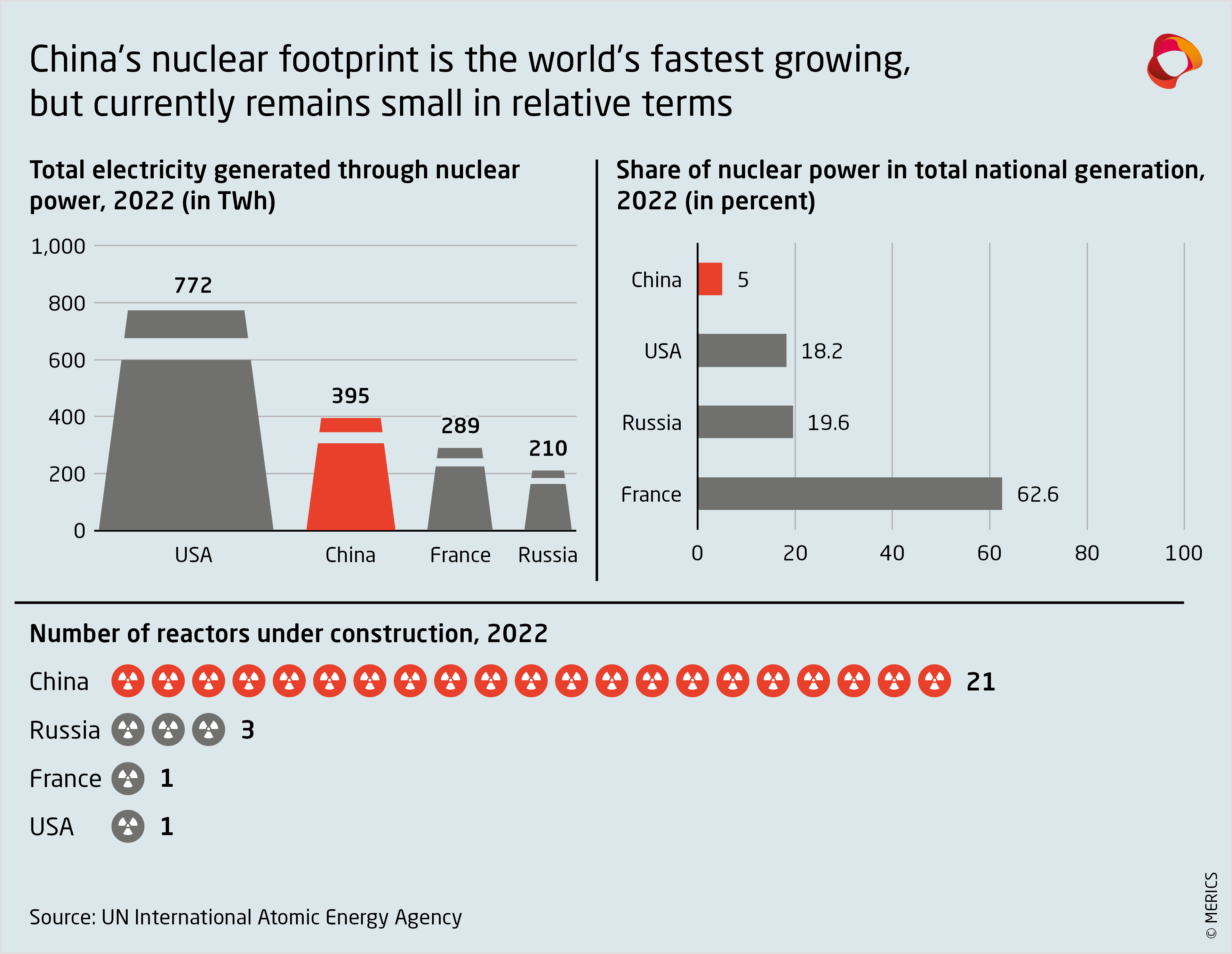

- Domestic demand occupies the bulk of industrial capacity – China is the world’s second largest generator of nuclear energy, but ranks 25th if nuclear energy is viewed as part of its national energy mix – a mere 5 percent of total generation. However, China has the most reactors under construction (21), far outstripping the second highest – India with 8. Domestic demand for new reactors already absorbs much of the industry’s production capacity, which in turn limits how much it can do overseas. Meanwhile, the major competitors have already built out their own domestic markets, so companies that grew in their home markets have spare capacity that they must push overseas to maintain momentum.

- China’s nuclear reactors lack the track record of their competitors – Many of China’s existing reactors either rely on outdated indigenous technology (that even China’s authorities no longer approve for new reactors) or foreign technology. With a few exceptions, such as several older Chinese model reactors in Pakistan, China’s own reactors have a limited record. The first Hualong One reactor only went online domestically in 2021. While plenty of Hualong One reactors are already committed to overseas, its relatively untested status may well be holding back other countries that may be eager to partner with China once the reactor is more proven.

China’s overseas nuclear energy footprint has potential but faces sizeable pitfalls

There is space for China’s nuclear energy champions to expand considerably overseas once the factors limiting their global growth resolve themselves. But the global dynamics of the energy transition could shift, new technology could expand global demand, and newer, more efficient alternatives to nuclear and carbon may emerge.

First, global demand for nuclear energy production could fluctuate considerably. While some European countries, notably Germany, seem even more committed to denuclearization than they are to decarbonization, others still see nuclear as a clean and reliable part of a decarbonized energy mix. The worldwide picture is complex, with countries taking a wide spectrum of views on nuclear energy. The more countries that opt-in to nuclear within their base-line energy mix, the more opportunities may open up for China’s players, though the inverse is also true.

Second, China’s nuclear industry is investing heavily in small modular reactor (SMR) technologies. The CNNC-designed ACP100 was the first successful land-based SMR to go into operation. The aim is to create a safe alternative to large, centralized, multi-reactor power plants. Successfully applied at scale, SMRs would allow countries to adopt a more decentralized energy grid strategy to incorporate nuclear within regional energy mixes. SMRs would also drastically lower the cost threshold - big nuclear plants are too costly for many smaller and developing countries. If China corners the market as the only supplier of SMRs, it could be a strong competitive risk to foreign rivals.

Third, nuclear energy will have to compete with a range of established and emerging non-carbon energy sources. Nuclear energy has one of the most expensive base costs of all energy types in term of cost per unit of electricity generated. But its price is among the most stable and its generates consistent amounts of energy, irrespective of weather. However, public opinion can swing fast and strongly, as happened after the Fukushima disaster, and disrupt industry plans. Finally, China’s nuclear energy champions also engage in a many other types of energy development, which could result in cannibalization within and between companies over what projects they want to push.

China’s nuclear energy rise is unlikely to compete with European players in the immediate future

Europe is home to many of the top companies across the entire nuclear energy value chain. France has the biggest names in building and managing plants, but the whole value chain incorporates companies from many EU member-states – much in the same way that Germany’s automotive industry incorporates a pan-European supplier base. As such, competition risks emerging overseas concern the whole bloc.

The risk presented by China’s nuclear champions overseas is relatively low in the short to medium term, especially compared to fields where Chinese firms are exerting pressure in third markets, like EVs, 5G and digital tech. However, Chinese nuclear energy competition has a chance of steadily emerging over the next decade or two. Maintaining a competitive edge is therefore essential, but so too is developing broader strategies to compete, on reactors, but also on project financing in third markets through platforms like the EU’s Global Gateway.

Global China Inc. Updates

China Inc.’s political and diplomatic developments /BRI

President Xi forges closer bonds with Central Asian countries

In May, President Xi Jinping hosted the leaders of five Central Asian countries in Xi’an. He unveiled an expansive plan to enhance collaboration with these ex-Soviet states in fields such as infrastructure, development, trade, energy, and security. Within this initiative, President Xi announced CNY 26 billion (USD 3.7 billion) in new loans and grants to support Central Asian nations. The event coincided with the G7 summit, leading to speculation that China’s intention was to promote a more multipolar world and challenge the US-led international system. President Xi’s renewed focus on Central Asia, an area historically within Russia's sphere of influence, was read as a sign China is gaining on Russia in terms of influence and power dynamics in the region.

Chairman of the Bank of China visits Papua New Guinea

Bank of China chairman Ge Haijiao has visited Papua New Guinea (PNG) to seek an operating license in the Pacific island nation. With abundant natural resources but limited development, roughly three quarters of PNG’s 10 million people remain outside the banking system. Many small and medium-sized enterprises (SMEs) have yet to integrate into the formal economy. PNG Prime Minister James Marape acknowledged China’s remarkable economic growth and urged the Bank of China to address the gaps in his country’s banking sector. PNG is also pursuing US defense ties; US Secretary of State Antony Blinken's recently visited to sign a defense cooperation agreement. The move has brought domestic political criticism and student protests, amid concerns about entanglement in China-US strategic competition.

Digital, Health, and Technology

BYD recognized as a leader in EVs as China becomes world’s largest auto exporter

According to the latest e-mobility transition ranking by the International Council on Clean Transportation (ICCT), Tesla and BYD have emerged as frontrunners. The ICCT report evaluates the progress of the world's top 20 automakers in transitioning to electric vehicles. Tesla took the top spot, closely followed by Chinese manufacturer BYD. The ICCT’s did a comprehensive data analysis on six key markets – China, the EU, India, Japan, South Korea, and the United States – which account for 89 percent of sales. The 20 manufacturers assessed by the ICCT represented 65 percent of global sales in 2022. The ICCT said BYD was fast closing the gap with Tesla and described both companies as leaders in the field.

The UK removes surveillance equipment manufactured by Chinese companies

The UK has announced its decision to remove surveillance equipment manufactured by Chinese companies from sensitive government sites. Although the statement did not mention any firms, lawmakers had called for bans on security cameras produced by Hikvision and Dahua. It follows previous UK actions, such as barring TikTok from government phones in March and announcing a ban on Huawei’s involvement in its 5G network in 2020. Beijing has expressed strong opposition to what it perceives as an expansion of the concept of national security to suppress Chinese enterprises.

Energy, Resources, and Commodities

The Philippines’ leading mining company is diversifying away from China

To reduce reliance on the Chinese market, Semirara, the largest coal miner in the Philippines, is shifting its focus towards the Japanese market. While China remains a significant foreign buyer, Semirara aims to expand its presence in other Asian markets. Semirara’s Chief Operating Office noted the slower-than-expected growth in Chinese industrial output. The change in direction is further supported by a significant decline in coal shipments to China, which dropped by 50 percent from January to March, reaching a total of 1.1 million tonnes. Semirara’s diversification seeks to mitigate risks from over-dependence on a single market and capitalize on growth opportunities elsewhere in Asia.

Manufacturing and Construction

Battery maker Gotion explores new market opportunities in Morocco

Chinese battery manufacturer Gotion High Tech has reached an agreement with Morocco’s government to explore setting up an electric vehicle battery plant there, with an investment of up to USD 6.3 billion over time. Reports suggest the factory could have a production capacity of 100 gigawatts (GW). Morocco already has a well-developed automotive sector that includes Renault and Stellantis, and sources of essential raw materials for EVs, such as cobalt and phosphates. The automotive sector was the largest contributor Morocco’s industrial exports in 2022, amounting to USD 11.1 billion.

Semcorp set to begin production in Hungary

Semcorp, a prominent Chinese battery supply chain leader, expects to start production in Hungary this year as its new factory is nearing completion. The facility has received 240 million euros in investment. Semcorp makes separators which prevent electrodes from shorting and overheating. In 2022, it manufactured 7 billion square meters of separators and wants to have production capacity for 16 billion square meters of separators by 2025. The Hungarian factory represents a significant expansion of its global presence.

Chinese and Thai companies collaborate to manufacture EV batteries

SAIC Motor-CP and Thai conglomerate Charoen Pokphand Group have formed a joint venture to build an industrial complex in Thailand making lithium-ion batteries and other electric vehicle (EV) components. Construction on the USD 14.9 million project began in April and will take until 2025. The site will also make parts for plug-in hybrids and fuel cell vehicles. Japanese automakers have dominated Thailand’s market but Chinese companies are now seeking to capture market share by setting up local EV manufacturing capabilities.

Hozon expands Electric Vehicle manufacturing to Thailand

China’s Hozon New Energy Automobile has announced plans to manufacture EVs in Thailand for the southeast Asian market. It signed an agreement with Thailand’s Bangchan General Assembly in May for production of its NETA V model, with a launch date of 2024. Other Chinese automakers such as BYD and Changan have also invested in manufacturing facilities in Thailand to benefit from its status as an automotive hub.

Trade and Finance

Bangladesh and Argentina embrace transaction in Chinese yuan

Bangladesh has found a way to meet its outstanding payment obligations to Russia for the Rooppur nuclear power plant (still under construction) by paying in Chinese yuan. Sanctions prevented Bangladesh from paying in US dollars, or Russian roubles. Stalled payments amounted to USD 110 million. Meanwhile, in April, the Argentinian government said it would start paying for Chinese imports in yuan instead of US dollars. It plans to transition to paying for approximately USD 1 billion of Chinese imports in yuan, followed by around USD 790 million of monthly imports. These developments are part of a shift towards embracing alternative currencies, particularly the yuan, in international trade transactions and pose challenges to dominance of Western-led financial institutions.

China’s trade is shifting toward emerging market

Qingdao Port in eastern China has unveiled 38 new shipping routes in the last 12 months, mainly to BRI countries. Much of Qingdao’s container traffic is intermediate materials, which are semi-finished articles used to produce manufactured goods and capital items such as machinery and tools. In contrast, Shanghai had a 6.4 percent decline in container volumes in the last quarter. Shanghai predominantly ships consumer exports to North America and Europe. The contrast suggests diversification toward emerging market destinations and a shift in the types of products China trades.

Transport and Logistics

Complications and delays plague Indonesia’s flagship BRI high speed rail project

The high-speed Jakarta-Bandung rail line, has hit fresh problems. The prominent BRI project has cost overruns of USD 1.2 billion and is four years behind schedule, partly due to work stopping during the Covid-19 pandemic. Indonesia’s transport ministry has now proposed delaying the commercial launch from August to January 2024. Financial restructuring at PT Wijaya Kaya Tbk (WIKA), an Indonesian state-owned construction firm with a minority stake in the consortium, is also complicating matters by impacting the project’s working capital requirements. WIKA has outstanding payments of at least USD 381.75 million and is seeking compensation for work already completed. Indonesia is currently in negotiations with China for an additional loan of USD 560 million and seeking a lower interest rate of 2.8 percent for the portion denominated in yuan while China Development Bank (CDB) is asking for 3.46 percent.

“Homegrown” Chinese passenger plane enters the market

China’s first homegrown large passenger jet, the C919, completed its maiden commercial flight on May 28th. For state-owned aerospace firm Commercial Aviation Corporation of China (COMAC), the C919 is part an attempt to position itself alongside giants like Airbus and Boeing, though that remains a long-term endeavor. Just a few months ago Japanese manufacturing giant Mitsubishi abandoned its 15-year effort to create a regional jet. The C919 plane can take 192 passengers and fly up to 5,550 kilometers. Chinese media says about 40 percent of the plane’s parts are imported, but industry experts say the real figure is higher.

China's shipbuilders expand into cruise ships

China’s first domestically-built large cruise liner, the Adora Magic City, sailed from Shanghai on a series of sea trials. The liner weighs more than 135,500 tonnes, has over 2,000 rooms and can accommodate up to 5,246 passengers. China is also building its second cruise ship, the H1509, which be longer and have more guest rooms. It represents another step toward greater industrial self-reliance, reaffirming China’s commitment to technological advancement and high-quality manufacturing.

Author(s)

Head of Program

Former Analyst

Former Senior Economist (Brussels office)

Former Analyst (Brussels office)

Author(s)

Head of Program

Former Analyst

Former Senior Economist (Brussels office)

Former Analyst (Brussels office)