picture alliance / CFOTO

Tracker

China Global Competition Tracker

The Digital Silk Road: A growing priority for Beijing as its tech champions expand overseas

No. 1, March 2024

The Digital Silk Road: A growing priority for Beijing as its tech champions expand overseas

European companies face growing competition from China’s digital champions in the Global South. Europe should do more to engage in digital project development overseas and support the competitiveness of European players. Finally off the ground after an underwhelming start, the Global Gateway – the EU’s global infrastructure initiative – has started to deliver some results in that direction. But it will be important to sustain that momentum as China’s role in wiring the world and forging tech partnerships is only poised to intensify.

In the Belt and Road Initiative’s (BRI) second decade, the focus is on smaller infrastructure projects involving new technologies, especially digital, that bring a good return on investment and promote Chinese firms overseas. The ‘Digital Silk Road’ (DSR), or the technology-focused leg of the BRI which exists alongside ports, rail, energy and roads, will therefore become more prominent, especially across the Global South. Not only are these key growth markets, but it will be important for China’s digital giants to expand overseas as they finish building out networks in China.

To better understand Chinese tech firms within the DSR, it is important to look at the factors pushing them overseas. Some, like Huawei and Bytedance, have been much written about. Here, we look at less well-known players in sectors such as undersea cables, AI, gaming and social media and ridesharing.

We found pressures for international expansion differed dramatically between consumer internet firms and China’s major players in the hardware and ‘real economy’ fields. Consumer-focused firms face a profit crunch in domestic markets that has sent them seeking growth markets elsewhere, whereas the hardware giants enjoy Beijing’s backing in the form of subsidies and project finance. At the same time, Beijing does welcome Big Tech investing abroad if that helps China dominate strategic technologies like artificial intelligence (AI), or at least generates revenue and profit that can be used to fund the right kind of R&D back home.

The importance of more “neutral” markets for China’s digital champions is growing as the tech rivalry with the United States has brought greater scrutiny of them in North America, parts of Europe and the Western Pacific. Besides, the domestic and emerging markets were often already more important. According to one analysis, for Huawei’s radio access network (RAN) business “any decline in European low-margin markets was offset in absolute terms by China and the emerging economies”.

Chinese telecommunication firms will therefore keep their focus on developing and emerging markets, whose governments are keen on digitally enabled solutions to development challenges ranging from public health to energy storage. In considering the pace of change, it is also worth acknowledging that geopolitical tensions and US controls on the export of semiconductor technology to China have not meaningfully slowed down the DSR—in fact, Huawei has managed to keep its carrier business afloat.

The DSR’s evolution will also depend on Beijing’s fiscal ability to support it amid deep structural constraints on the economy and financial system. The China International Contractors Association has found big ticket projects becoming rarer as the average value of BRI projects dropped 24.8 percent between the 2013-2017 period and 2018-2022, though the number of projects grew by 89.6 percent.

Nevertheless, Beijing continues to see digital development as an important growth driver. At the 3rd Belt and Road Forum in October 2023, it launched two initiatives to encourage international cooperation on the digital economy, namely the Beijing Initiative on the Belt and Road International Digital Economy Cooperation and the International Trade and Economic Cooperation Framework for Digital Economy and Green Development.

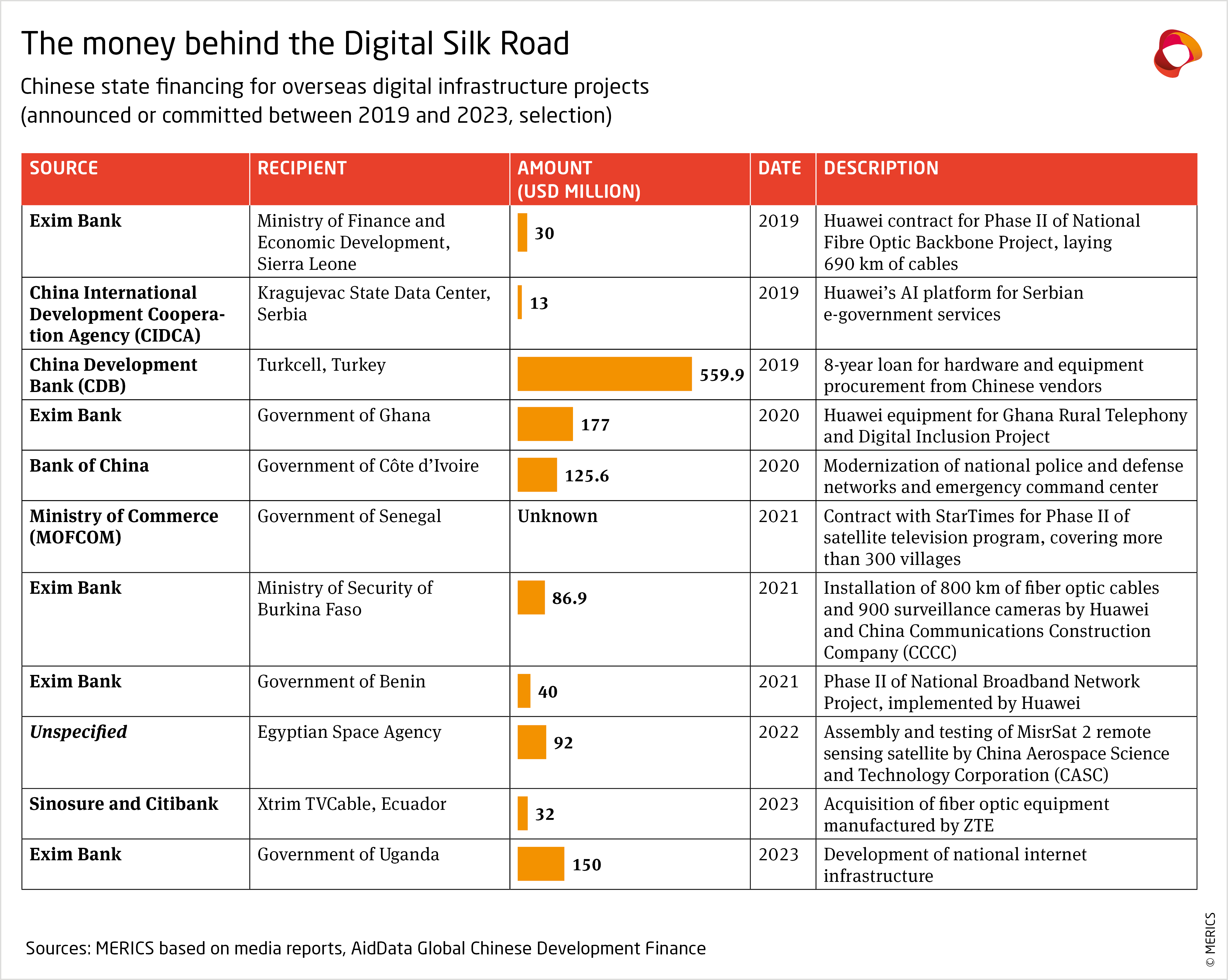

Digital infrastructure projects are also cheaper. Although the multi-billion export credit lines of the past are now rarer, anecdotal evidence suggests state financial support is still coming in. It supplements commercial investments and partnerships, which are more organic.

Beijing encourages favored champions to go abroad

China’s government essentially views the DSR as the outward-facing support to domestic efforts to digitalize the “real economy”. It continues to create favorable conditions for Chinese technology companies, both state-owned and private, to facilitate their internationalization. While the former receive direct state support, the latter are encouraged to pursue commercial opportunities abroad where it fits Beijing’s strategic goal of emerging technology leadership.

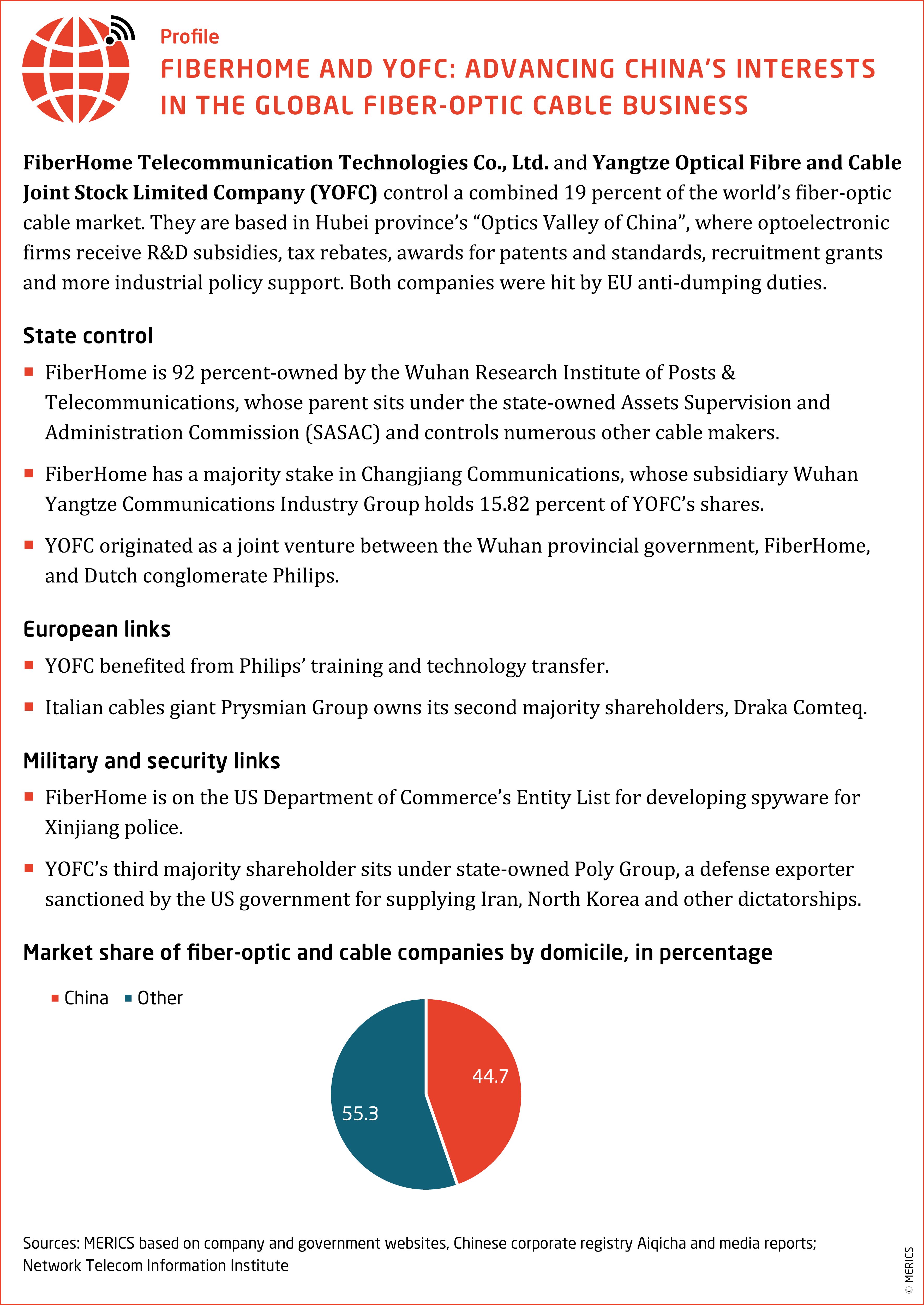

Controversial PRC undersea cable makers enjoy ample state support

The fiber optic cable sector illustrates the DSR’s drivers, logic and implementation. Ocean-floor telecommunications infrastructure carries over 95 percent of international data traffic. Unsurprisingly, it has featured in Beijing’s infrastructure foreign policy documents ever since the first mentions of the DSR in 2015. The global rise of Chinese undersea cable makers shows how Beijing helps national champions compete in third markets and raises security concerns.

The meteoric rise of Huawei’s submarine cable division first triggered US worries about the risk of data exfiltration and manipulation. In 2020, it was sold to Hengtong Optic-Electric, a subsidiary of private conglomerate Hengtong Group, and rebranded HMN Technologies. Between 2019 and 2023, HMNT was the fourth most active supplier globally by number of systems installed, ahead of the Italian Prysmian Group. Nokia’s Alcatel Submarine Networks (ASN) kept a strong lead, followed by SubCom and NEC. Moreover, HMNT’s new parent, Hengtong has been making overseas acquisitions and majority investments in the past decade, including in Portuguese Alcobre, Spanish CABLESCOM, and German J-Fiber.

Huawei’s exit did not calm security concerns, given Hengtong’s involvement in Military-Civil Fusion (MCF) programs. It built a dual-use undersea surveillance network in the East and South China Seas and has links to an entity affiliated to military cyber intelligence. Other Chinese cable makers and operators include Jiangsu Zhongtian Technology (ZTT), which is also involved in dual-use undersea monitoring projects and was praised by President Xi Jinping for its contribution to national defense, and a cable in the Baltic Sea belongs to a company owned by China’s Ministry of Finance.

Fiber is earmarked for industrial policy support in the Made in China 2025 plan, and Beijing sees a double opportunity, to export domestic overcapacity into third markets and promote national champions. With HMNT, Hengtong inherited a heavily subsidized player which has been able to place cheap bids, likely thanks to Chinese policy bank export financing. A number of Chinese optical fiber cable exporters were hit by European Commission dumping duties, measures that were tightened in 2023.

In 2021, Hengtong Optic-Electric introduced a manufacturing fund under China Development Bank along with two other strategic investors, and last year HMNT signed a strategic cooperation agreement with Sinosure, the state-backed export credit insurance company. Beside supporting cable installers, China Inc. also helps producers compete in third markets (see Exhibit ‘Profile: Fiberhome and YOFC’).

Awareness of the strategic vulnerability of undersea information corridors is growing. Undersea cables have also become a battleground of US-China competition. US authorities have blocked some cable projects and pushed Chinese firms out of others, e.g., the South East Asia-Middle East-West Europe 6 project. In January 2024, the European Parliament passed a resolution calling for better protection of critical infrastructure from Chinese state influence.

Shortly afterwards, as part of its de-risking work stream, the European Commission recommended several actions for reducing dependencies on “high-risk suppliers” and financing secure alternatives.

Chinese AI companies seek markets and research partners abroad

China’s official blueprint for AI development encourages AI firms to expand abroad. The 2017 New Generation AI Development Plan pledges to “support cooperation between domestic AI enterprises and leading international AI schools, scientific research institutes and teams”. AI companies are promised assistance with foreign mergers or acquisitions, stock investments, startup investments and establishing overseas R&D centers. The plan calls for AI adoption through the BRI.

The Middle East has become a testing ground for these ambitions. Chinese AI company SenseTime entered a USD 270 million collaboration in 2022 with the Saudi Company for AI (part of its sovereign wealth fund) and trains AI talent there. SenseTime and Alibaba both have smart city contracts for the planned new Saudi metropolis of Neom. The Financial Times cited SenseTime’s “slumping share price and falling revenues from its core domestic surveillance business” as reasons for expansion. Alibaba has also been leveraging its growing cloud business in the Middle East to sell AI applications for public sector digitalization.

Chinese firms are strong in large language models (LLMs), including generative AI models; as several of these are open source, they may soon begin to be adopted abroad. For example, Alibaba’s DAMO Academy has been working on southeast Asian languages to develop AI for the region. In Saudi Arabia, King Abdullah University of Science and Technology (KAUST) has launched the Arabic-focused model AceGPT, which is built on Meta’s Llama 2. KAUST’s project partners are The Chinese University of Hong Kong and the Shenzhen Research Institute of Big Data.

These partnerships have sparked scrutiny in Washington amid fears that Chinese firms might use them to circumvent export controls on elements of supercomputers. The United States sought to close these loopholes in October 2023 by expanding US semiconductor export controls aimed at China to certain third countries and subsidiaries. Abu Dahbi-based company G42 recently found itself caught in the middle and gave up some China links to appease US authorities.

European AI firms and universities may soon face similar dilemmas. British AI chip designer Graphcore pulled out of China in November 2023, citing US export controls. European start-ups in the semiconductor space report similar pressures and wonder how to achieve scale without selling into China’s USD 179.5 billion semiconductor market. Strong ties between Europe and China in AI research mean academia will face challenges recalibrating collaborations, especially as the EU slowly but steadily embraces “de-risking” in critical technology sectors.

Consumer internet giants go overseas to compensate for lost ground at home

Unlike China’s well-favored tech champions, players in consumer sectors are expanding overseas to counter diminished opportunities at home. Many were mauled by Beijing’s rectification crackdown on the digital sector between 2020-2022, notably entertainment giant Tencent and ride-hailing service Didi Chuxing.

Both Didi and Tencent faced a political and regulatory storm that combined antitrust rules; the then-new Cybersecurity Law, Data Security Law, and Personal Information Protection Law (hereafter the “cyber and data regime”), new industry-specific regulation and old-fashioned political campaigns like that targeting private sector billionaires like Jack Ma.

Tencent has been so undercut at home that growth abroad is critical

All the internet giants took a big hit, but Tencent suffered blows that are likely to last longest. Its main business sectors – gaming, social media, and media content – are in areas Beijing objects to most: they create real and imagined social ills and deflect innovators from working on the ‘real economy’.

- Tencent was found in violation of anti-monopoly transaction disclosure rules and charged with 12 violations of the Anti-Monopoly Law.

- Tencent’s proposed M&A merging the Douyu and Huya live-streaming services, focused on gaming, was blocked.

- Tencent surrendered a ‘golden share’ to a party state entity, granting the holder special voting and veto rights. The reported intent was for the party-state to have a hand in steering decisions related to data and content management.

- Tencent has been undermined by regulatory decisions big and small. In 2021, a nine-month freeze on new game licenses caused major problems. The number of games approved since remains far fewer than before. Scrutiny of certain types of revenue like in-game microtransactions was less devastating but still impactful.

Hamstrung in its home market, Tencent has actively pursued internationalization. Beijing disapproves of gaming and social media as the focus for one of its most innovative companies. Nor does it want Chinese citizens wasting much time on these entertainments. But it is far less opposed to Tencent going overseas for growth markets.

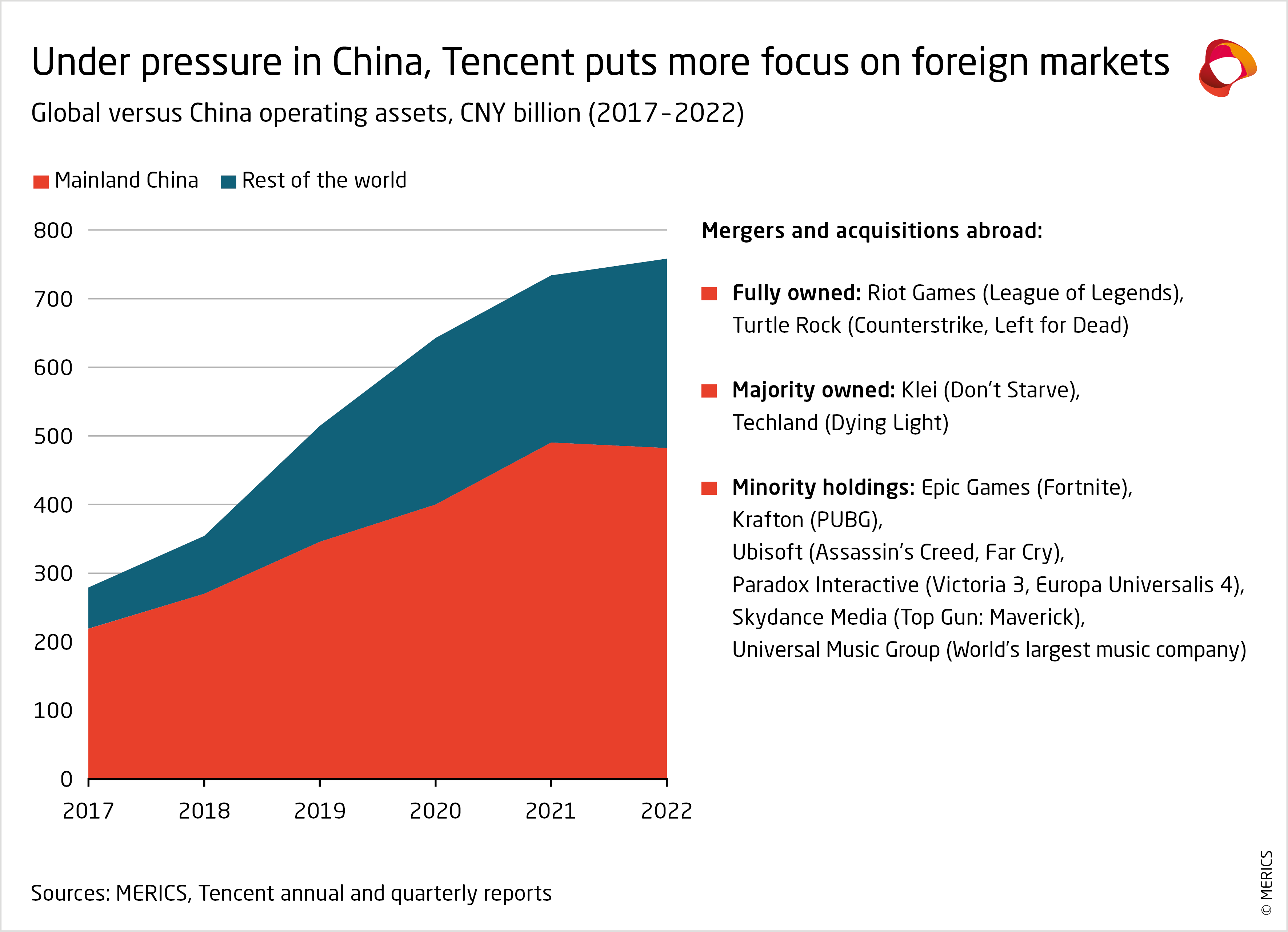

Tencent has focused on overseas expansion for several years now, especially in gaming, but also in e-commerce, music, and film. It would prefer full ownership or majority-ownership. Yet, it has taken minority stakes where it can in its eagerness to build up global revenue streams. These will take some time. Tencent must first build up market share. It would take a lot to replace the massive Chinese gaming market and the kinds of profits they could derive there prior to the crackdowns.

In 2022, Tencent’s overseas revenue was only one tenth of that generated in China and its domestic product offering far more varied. However, its international revenues (primarily gaming-focused) have grown much faster in relative terms. From 2017 to 2022, Tencent more than doubled its domestic revenues, from RMB 230 billion to RMB 503 billion, yet overseas revenue rose six and a half times, from RMB 8 billion to RMB 52 billion.

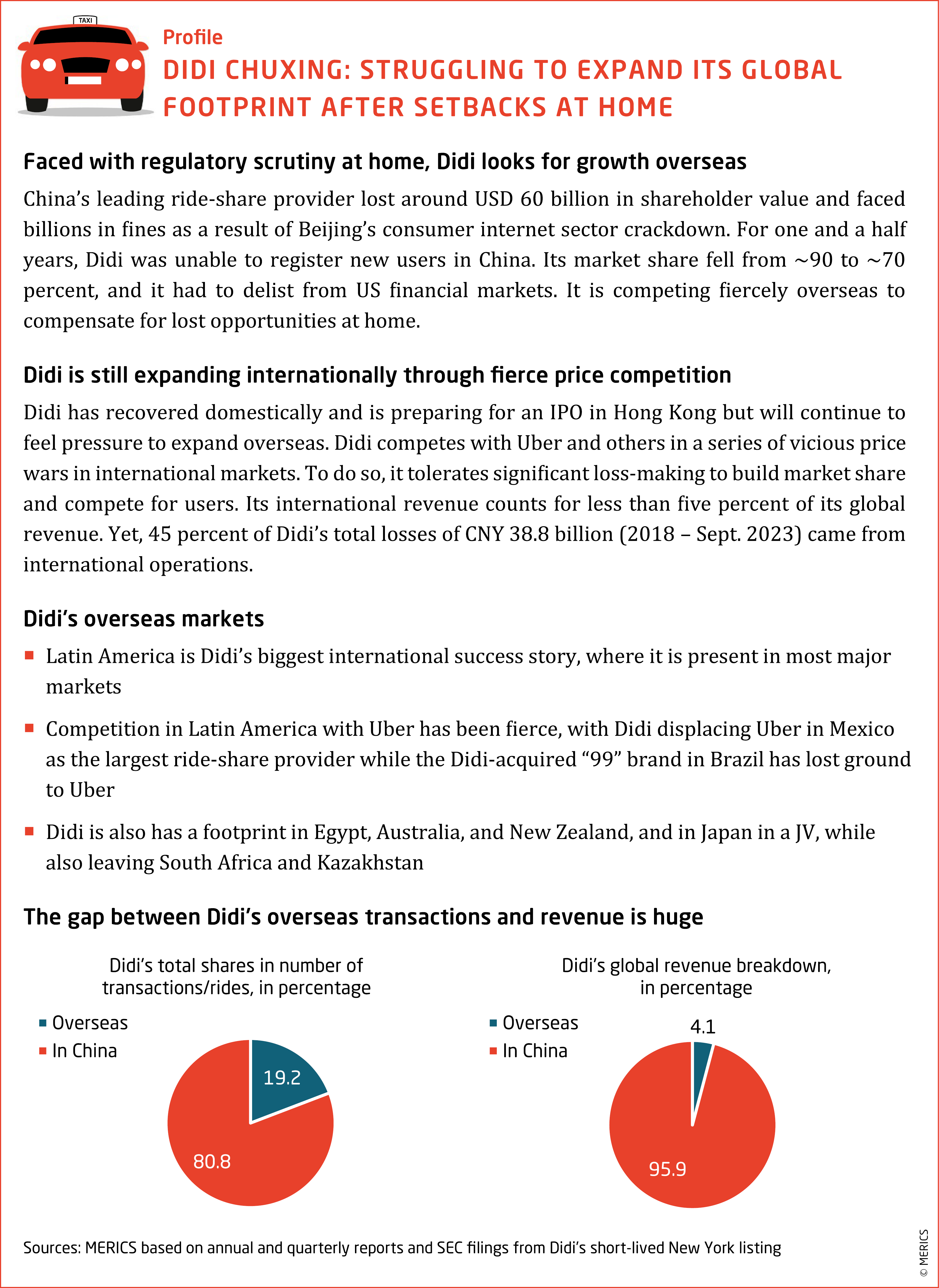

Didi is struggling to expand in new growth markets after setbacks at home

Didi Chuxing, China’s leading ride-share provider which defeated then bought Uber’s China operations, took major blows in the aforementioned consumer internet sector crackdown by Beijing. It lost around USD 60 billion in shareholder value and faced billions in fines, eventually heaping enough pressure on the firm that it delisted from US financial markets at the end of 2021. (It’s IPO earlier that year is widely regarded to be the trigger point for Beijing’s crackdown on the firm).

As Didi recovers domestically and prepares for an IPO in Hong Kong, their home market position is likely to stabilize. However, new growth in the tapped-out China market and under the new regulatory and political conditions there will have limits, which will continue to add to pressure to expand overseas.

Outlook: China’s digital giants will keep internationalizing

Going global is increasingly a necessity for China’s digital champions. It will continue, either thanks to government support, or because companies are seeking growth outside of a China that is no longer the market it once was. Whether the favored digital champions or the disfavored, Chinese firms are set to be major players facilitating the digital transition in much of the developing world.

European governments would do well to understand the speed and scope of the DSR and consider what is required for Europe to compete. What is needed in projects under initiatives like the EU’s Global Gateway, or the promising collaborative efforts within the transatlantic Trade and Technology Council (TTC) framework and with other partners like Japan. The involvement of the European Investment Bank and the European Bank for Infrastructure and Development in subsea cable financing is an encouraging step.

Some European companies are well positioned to compete with Chinese firms in enabling digital connectivity and technology adoption in third markets. However, it will be an uphill battle where Beijing’s support for Chinese firms in those markets, either financially or otherwise, skews the playing field for European firms.

The fact that Europe lacks hyper-scalers, like Alibaba or Alphabet, will not make things easier. This is exactly why the European Commission is encouraging member states to up their level of ambition – for example, by mobilizing industrial policy and fund secure undersea connectivity. Importantly, the sooner that Europe can meaningfully compete with the DSR, the better, as the longer that China’s digital champions have to build up market share relatively unopposed, the harder it will be for European firms to compete and chip away at China’s established positions.

Global China Inc. Updates

BRI Politics and Trade

China and Lithium

China's Tsingshan Holding Group is set to make a significant investment of USD 233.2 million to establish a lithium iron phosphate (LFP) production facility in northern Chile. It aims to be operational by May 2025 and to produce 120,000 metric tons of LFP annually. Sinomine recently completed a major USD 300 million upgrade of Zimbabwe's largest lithium mine. Zimbabwe, home to Africa's largest lithium reserves, wants to reach a mining output value of USD 12 billion.

BRI: China-Arab cooperation

China has signed BRI cooperation documents with all 22 Arab nations and the League of Arab States, following a recent BRI pact between China and Jordan. Over the past decade, bilateral trade between China and Arab countries has doubled, surpassing USD 430 billion in 2023.

Transport and Logistics

USD 1.5 billion port deal in Sri Lanka

Hunan Construction Investment Group signed a USD 1.56 billion four-party agreement on investment cooperation for the Phase 2 of the Colombo Port City, Sri Lanka.

City rail in the DRC

Chinese company Sinohydro has signed a contract worth USD 834 million, with Trans Connexion Congo to build the third part of Kinshasa’s urban rail system in the Democratic Republic of Congo (DRC) and supply the trains. The 90-kilometer circular line is the longest of four new urban rail lines for Kinshasa.

Manufacturing and Construction

CATL and BYD Dominate the Global EV Market

China's EV industry battery giants CATL and BYD together dominate over half of the global EV battery market. CATL’s global market share was 36.8 percent in 2023, and BYD’s was 15.8 percent, while CATL expanded its battery production capacity 40.8 percent to 259.7 GWh and BYD increased its power battery installations to 111.4 GWh in 2023, an annual rise of 57.9 percent.

Chinese service robot makers target overseas markets

Chinese service robot makers are expanding into international markets, leveraging early market entry and competitive pricing. Keenon Robotics reported higher earnings overseas than at home, signaling growth potential, while Pudu Technology now supplies 80 percent of Japan's catering robots.

Energy, resources, and commodities

Copper mines in Botswana and Ecuador

Chinese state-owned mining conglomerate MMG has secured control of Botswana’s Khoemacau copper mine by acquiring Cuprous Capital Ltd and aims to triple production from 50,000 tons per year to 155,000 tons. Ecuador’s government has also granted a copper mining expansion permit, to China's Tongling Non-Ferrous Metals for the Mirador mine, permitting annual output to rise from 120,000 tons to over 200,000 tons with additional investment of USD 650 million.

China's presence in Serbia's energy infrastructure is growing

In the renewable energy sector, Power China has acquired a 51 percent stake in Serbia's Vetrozelena wind project, backed by a favorable Power Purchase Agreement (PPA) with Serbia's national power company. CEEC Jiangsu has completed a new coal-fired power unit in Serbia, despite regulatory challenges and public opposition.

Chinese mining deal in DRC

Construction firms Sinohydro Corp and China Railway Group have agreed to increase investment in their Sicomines copper and cobalt joint venture in DR Congo from USD 3 billion to USD 7 billion after President Felix Tshisekedi's government revisited the initial deal to address concerns about inequity. The deal maintains the current shareholding structure, with the Chinese partners agreeing to pay 1.2 percent of royalties annually to DR Congo.

Trade and finance

Free trade agreement between Ecuador and China

Ecuador ratified a Free Trade Agreement with China on February 7, making it fifth Latin American country to have such an agreement; China’s similar deals with El Salvador, Brazil, Argentina and Nicaragua include settling imports in Chinese yuan. China has become increasingly active in the region which traditionally has strong US links. China’s trade volume to Latin America grew from USD 8.5 billion in 2000 to USD 180 billion in 2020.

Trade deal with Switzerland

On January 16, China announced a unilateral visa-free entry policy for Swiss citizens, after discussions between Chinese Premier Li Qiang and Swiss President Viola Amherd. There are plans to upgrade the China-Switzerland Free Trade Agreement (FTA), with formal negotiations on the horizon.

Uzbekistan: Chinese company granted RMB-denominated power purchase agreement

Uzbek representatives signed a Power Purchase Agreement (PPA) with Universal Energy, a Chinese company, for a 500MW wind power project. All payments will be in Chinese yuan, making the project more attractive for Universal Energy.

PBOC fines S&P China and 5 other rating agencies a total of USD 4.5 Million

The People’s Bank of China (PBOC) has imposed fines totaling RMB 34.5 million (USD 4.8 million) on six credit rating agencies, including S&P Global Ratings' Chinese subsidiary and five domestic credit ratings agencies. The fines were for multiple violations of regulatory rules: S&P China was fined USD 297.000.

Author(s)

Head of Program

Head of Program (Co-lead)

Author(s)

Head of Program

Head of Program (Co-lead)